Abstract

How to build a sustainable seaweed industry is important in Europe’s quest to produce 8 million tons of seaweed by 2030. Based on interviews with industry representatives and an expert-workshop, we developed an interdisciplinary roadmap that addresses sustainable development holistically. We argue that sustainable practices must leverage synergies with existing industries (e.g. IMTA systems, offshore wind farms), as the industry develops beyond experimental cultivation towards economic viability.

Similar content being viewed by others

Introduction

Seaweed farming is gaining global attention as a sustainable solution for restorative aquaculture1. While Asia farms 99% of the global marketed seaweed, and produces 34.7 million tons annually worth 14.85 billion USD2, Europe’s seaweed industry is yet mostly run by startups3. European farmers produced only 3.8% of the 287,033 tons harvested in 2019, with most production coming from wild stocks4. As of today, seaweed farming plays a key role in the EU’s strategic guidelines for sustainable aquaculture5. Cold temperate regions, from Norway to Portugal, offer ideal conditions for seaweed cultivation6. Norway’s leading position in Europe’s seaweed production2, with 44 seaweed-related companies, hinges on the wild harvests of 150,000–200,000 tons annually of Laminaria hyperborea and Ascophyllum nodosum (Phaeophyceae) to produce alginate6,7. Commercial farming is yet small-scale, with a peak production of 600 tons in 20238, and focuses on the kelps Saccharina latissima and Alaria esculenta (Phaeophyceae). In Portugal, 16 smaller businesses (phyconomy.org, accessed June 2023), alongside the leading company AlgaPlus, complement the European seaweed sector with species that thrive in warmer conditions, like Porphyra sp. (Rhodophyta), Fucus spiralis, Laminaria ochroleuca (Phaeophyceae), Ulva sp. (Chlorophyta), and Gelidium sp. (Rhodophyta)9.

The European seaweed industry faces challenges, such as high production costs, limited infrastructure, regulatory hurdles including complex licensing procedures, and the need for consistent, high-quality biomass to meet market demands10. Unlike Asia, where selective breeding programs have optimized traits for yield11, Europe largely relies on wild stocks for seed material. Additionally, a mismatch between cultivated species (Alaria esculenta, Saccharina latissima) and market demand (Palmaria palmata, Undaria pinnatifida)12), high production costs13, and knowledge gaps in environmental impact14, further hinder expansion of the European seaweed industry. Addressing these challenges through selective breeding, improved seedstock, and technological innovations could enhance sustainability, resilience, and economic viability in the European seaweed sector.

Seaweed farming does not rely on farmland, feed, fertilizers (at least on small farms), antibiotics, or pesticides. Seaweeds absorb carbon, nutrients, and heavy metals, support marine food webs, and provide habitats to a variety of marine organisms15,16,17 – yet on a smaller scale than wild kelp forests. Moreover, seaweed farming aligns with 13 of the UN’s 17 Sustainable Development Goals (SDGs)18,19,20,21,22,23. Therefore, at current production levels, seaweed farming is regarded as a sustainable blue economy, with minimal negative impacts24.

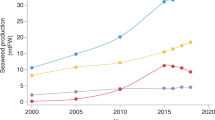

By 2030, the European Commission aims to increase production to 8 million tons, valued at 9 billion Euros, and potentially creating 85,000 jobs25 (Fig. 1). Such a 30-fold increase in farmed production over a decade raises concerns about sustainability thresholds. Intensive seaweed farming could exhaust nutrients in oligotrophic regions, as observed in China, where enhanced nutrient uptake by kelp farms has led to a decline in phytoplankton populations and disruptions in marine food webs26.

Projected expansion of Europe’s farmed seaweed production in volume and market value through 2030, compared to global developments. a Projected seaweed production volume (in million tons wet weight) in Europe and other regions. b Projected market value of seaweed (in billions of USD) in Europe versus other regions. The category labeled ‘Other’ is primarily driven by Asian countries. Historical data were sourced from the FAO Fisheries and Aquaculture database (online query). Projections for Europe are based on25, and global projections are based on126 for volume, and on127 for market value. Growth is estimated using compound annual growth rate (CAGR). EU refers to the European Union, and FAO to the Food and Agriculture Organization of the United Nations.

Intensive farming also increases the deposit excessive organic matter leading to hypoxic conditions on the seafloor, as documented in Sanggou Bay, where sediment analysis revealed shifts in benthic community structure due to long-term kelp farming27. Moreover, reduced light penetration under seaweed farms can, lead to changes in marine environments28,29,30.

Other risks include the spread of non-native species, seaweed diseases, and over-exploitation of wild seaweed beds for seeds28. Large-scale monocultures of fast-growing strains can further reduce biodiversity, and increase vulnerability to diseases29. In China and Korea, Saccharina japonica and Undaria pinnatifida cultivation has led to genetic homogenization, with some farmed strains escaping and interbreeding with wild populations31,32. While controlled breeding programs have helped maintain genetic distinctness in some cases, the unintended release of spores from farms has contributed to genetic introgression in wild stocks11. At the societal level, the seaweed industry may conflict with established local maritime activities such as fisheries and tourism, and fail to benefit local communities.

The sustainable growth of the seaweed industry relies on three interlinked pillars: (1) the environmental pillar, which emphasizes biodiversity impacts at all levels, from genes to ecosystems28,29,33,34, (2) the economic pillar, centered on profitability for farmers and stakeholders35, and (3) the social pillar, addressing social acceptance, job security, livelihoods, and community benefits36,37. A sustainable economy ideally balances these pillars, as it increasingly hinges on consumers’ trust through verifiable contributions to ecological and social sustainability38.

The EU’s new 2021 directive on sustainability reporting39 now requires large companies to verify their claims of sustainable production. Sustainability, rather than being viewed in the traditional perspective of linear thinking as a static goal40,41,42, is an evolving process, continually shaped by new knowledge and development43,44. An emerging inclusive approach to sustainability is the “One Health” initiative, which links human, animal, and environmental health45. While the Blue Bioeconomy Forum offers general guidance for sustainable production46, seaweed farmers, hatcheries, and political bodies require more specific strategies. To provide guidance, we developed a seven-step roadmap to establish sustainable transformations for the seaweed sector. Through stakeholder interviews and a workshop with Norwegian and Portuguese partners, we identified focus areas that balance environmental, economic, and social aspects to position Europe’s seaweed industry as a role model of a sustainable blue economy.

Methodological approach

Tools that can assess sustainable practices fall into six categories47: (a) participatory tools, (b) scenario analysis tools, (c) multi-criteria analysis tools, (d) cost-benefit analyses, (e) accounting tools, physical analysis tools, and indicator sets, and (f) model tools. Tools (a) and (b) form the foundation on which tools (c)–(f) can be followed for more detailed assessments47.

Participatory tools involve stakeholders to articulate opportunities and challenges for sustainable development. We conducted 9 semi-structured interviews with industry representatives from Norway (N1–N5) and Portugal (P1–P4) in their native languages (guide in Supplementary File 1, and registrations in Supplementary File 2 and Supplementary File 3) via Teams, transcribed and translated them into English, and analyzed them with the RQDA R package48. These represent 11% of Norwegian stakeholders (5 of 44) and 25% of Portuguese stakeholders (4 of 16) registered as a seaweed company in the phyconomy database (phyconomy.org, accessed June 2023). While this sample provides valuable insights from two distinct regions in Europe, it does not fully capture the diversity of the entire European seaweed industry.

The interviews (guide in Supplementary File 1) covered key themes, including definitions and implementation of sustainability, regulatory frameworks, environmental, social, and economic impacts, and innovation priorities. The interviewees were asked about their experiences, sustainability strategies, and barriers to sustainable development. Discussions also explored potential improvements in industry collaboration, research integration, and policy support. The guide was flexible to ensure consistency while allowing participants to elaborate on their perspectives.

Backcasting distinguishes from other scenario analysis tools to identify pathways toward sustainability, by starting with a vision of an ideal future instead of the present limitations49. We implemented backcasting to draft a roadmap that bridges the gap between the ideal future by 2050 and the current state. In this process, we applied the “four-arrow model” template presented by Okada et al.50 because it explicitly links technological advancements with market needs while bridging the gap between the current state and a desired sustainable future (Fig. 2). We proceeded in 4 stages: 1) preparation, 2) development of a sustainable vision, 3) development of pathways to reach that vision, and 4) post-workshop analysis.

Overview of the methodological framework applied during the stakeholder workshop to develop a shared vision and actionable roadmap for a sustainable European seaweed industry. The process began with a a Futures Wheel exercise, where participants envisioned a desirable future state for the European seaweed industry in the year 2050 (right), and a SWOT analysis of the present state of the industry (left), identifying Strengths, Weaknesses, Opportunities, and Threats. b These inputs were structured into a “four-arrow” backcasting template, which organizes the transition from Present (left) through Gap (center) to Future (right). Each statement from the workshop was coded at one of three operational levels—Market, Product, or Technology. Within the Gap section, every statement was further classified into one of 40 specific roadmap categories that reflect actionable themes, and these were grouped into seven overarching roadmap steps (circled and numbered 1–7), representing the key areas for bridging the current state and the envisioned future. c Each colored dot represents a coded statement, assigned to one or more of the four sustainability dimensions defined by the Wheel of Sustainability (WOS): Environment (green), Economy (orange), Governance (purple), and Culture (blue). Statements that address multiple dimensions are indicated by multicolored dots. The WOS framework, adapted from Circles of Sustainability for the macroalgae sector, was used to ensure a comprehensive and interdisciplinary sustainability assessment throughout the roadmap development process.

1) Preparation: We invited 14 stakeholders from Norway and Portugal (8 men, 6 women; 9 from the natural sciences, 2 from the social sciences; 3 industry practitioners) to a three-day workshop at Nord University in 2022. The stakeholders represented the northern and southern limits of a variety of seaweed species, and seaweed farming practices6, and a variety of expertise areas within the United Nations’s sustainable development goals (SDGs) and the “Wheel of Sustainability” (WOS).

Given its demonstrated applicability to aquaculture and its emphasis on holistic sustainability evaluation, the WOS was chosen as the primary framework for structuring our sustainability assessment in the seaweed industry. The WOS provides a comprehensive framework for evaluating sustainability in aquaculture, extending beyond the commonly used triple bottom line (environmental, economic, and social sustainability) by incorporating governance and cultural aspects51 (Supplementary Fig. 1). The WOS was adapted from the Circles of Sustainability52 for salmon aquaculture to the macroalgae industry53, aligning it with the ASC-MSC Seaweed Standard, the only established sustainability certification specific to seaweed farming54. This adaptation acknowledged the positive environmental contributions of macroalgae farming, including e.g. carbon capture and water quality improvement in the context of broader sustainability challenges.

2) Development of a sustainable vision: To structure our vision of an ideal future state of the seaweed industry, we constructed a Futures Wheel55. The Futures Wheel structures brainstorming about second- and third-order impacts of future scenarios, such as consequences, impacts, possibilities, and expectations. The Futures Wheel has been widely used in sustainability and policy planning as it facilitates collective thinking on long-term consequences of innovations, regulatory changes, and industry shifts. Organizing individual ideas together in a group discussion (Supplementary Fig. 2), and transferring them to the right-hand side (future state) of the ‘four-arrow’ backcasting template (Fig. 2a)50 (Supplementary Fig. 3), ensured that our roadmap was built upon a shared and systematically developed vision, rather than an arbitrary set of assumptions.

3) Development of pathways to reach that vision: We first evaluated the current state of the seaweed industry with a SWOT analysis (strengths, weaknesses, opportunities, threats) (Supplementary Fig. 4), and transferred these to the left-hand side (current state) of the four-arrow backcasting template (Fig. 2, Supplementary Fig. 3). The workshop participants then identified the challenges and tasks to bridge the gap between the present and the envisioned future, and grouped all ideas into seven roadmap topics, which we transferred to the middle area (roadmap) of the ‘four-arrow’ backcasting template (Fig. 2, Supplementary Fig. 5).

4) To distill key action points and policy recommendations, we analyzed the interview and workshop content using the R package RQDA48. RQDA is a tool for qualitative data analysis that enables the systematic coding of text segments to user-defined categories. Thus, it allows for quantitative analysis based on the frequency of coded categories, and also allows for the extraction of qualitative statements that contextualize those quantitative assessments. We applied an integrated analysis for a comprehensive and interdisciplinary understanding of how to develop Europe’s seaweed industry sustainably. Although the interviews and the workshop were conducted as independent processes, we analyzed their content jointly using RQDA. All material was coded into 29 WOS categories (Supplementary Data 1), 40 roadmap categories, and 14 technology push/market pull categories (Fig. 2) following the framework of50. We then assessed the relative importance of each WOS subsection based on the frequency of mentions in both interviews and workshop discussions. While the interviews did not inform or structure the workshop activities, they offered complementary insights—particularly valuable in highlighting country-specific differences in how stakeholders prioritized the same or different aspects of sustainability. We extracted stakeholder quotes from the coded content to strengthen and exemplify the stakeholder perceptions that stand behind the quantitative results to enhance their robustness and validity. To identify synergies that address more than one sustainability goal—we extracted raw text that we had coded simultaneously to two or more WOS dimensions (e.g., environmental and economic). We then filtered these for recurring co-occurrences supported by more than three distinct statements, to highlight robust overlaps. This helped us pinpoint cross-cutting themes where addressing one aspect may benefit multiple dimensions of sustainability, such as ecological protection and community acceptance. We then visualized the interactions between the SWOT elements and their relationship with the roadmap and WOS dimensions using the alluvial R package56.

Results and discussion

Our approach to sustainable seaweed farming in Europe revealed the environmental and governmental aspects as most significant (Fig. 3). Key subsections, such as G6 (Coordination and Collaboration of Interests and Activities) and E2 (Biotic Effects), were among the five most frequently mentioned across interviews and workshop discussions, based on the RQDA-based frequency analysis (Fig. 3). The sustainability categories showed 33 interconnections across the WOS codes, each supported by more than 3 independent statements from the workshop or interviews (Supplementary Data 2). Governance appeared in all 7 of the most interconnected dimensions, each with ≥10 supporting statements (Table 1) and, was, together with the environmental focus the most important of the WOS dimensions (Fig. 3).

Comparison of how frequently different sustainability attributes were mentioned by stakeholders across three data sources: Interviews from Norway (left), Interviews from Portugal (center), and Workshop (right). Bars represent coded segments related to each sustainability attribute, grouped by Wheel of Sustainability (WOS) categories: C (Cultural = blue), E (Environmental = green), Ec (Economic = orange), and G (Governance = purple). Attributes are ordered top-to-bottom within each category based on total frequency across all three data sources. Frequencies are shown as percentages of total coded segments per source. Three attributes most consistently mentioned across datasets are highlighted. Arrows indicate mjor discrepancies in the representation of a topic among the interviews (C1, Ec3) or between the interviews and the workshop (C3).

Stakeholders’ understanding of sustainability

This section direclty builds on the quantitative analysis presented in Fig. 3, which outlines the relative importance of the WOS framework elements for Norwegian and Portuguese stakeholders. We first explore shared concerns—such as Environmental sustainability (E2, E5), and Community Contributions (C3)—and then contrast how specific elements such as Environmental Concerns (EC1) and Economic Costs (EC2) diverge between interviews in the two countries. Selected stakeholder quotes shall exemplify these themes and provide context to the patterns identified in the quantitative data.

Environmental sustainability (especially E2, E5) was an important factor for the farmers interviewed in Norway and Portugal (Fig. 3). As Portuguese interviewee P1 stated: “…we don’t think just about having to make as much money as possible as quickly as possible. We have to create a sustainable company that has the least possible impact”. Environmental sustainability was also identified as key driver in the development of the Scottish and Irish seaweed industries while large-scale multi-national companies were dismissed by all stakeholders57,58. While our findings align with broader sustainability trends in the European seaweed sector, research across other countries is needed to confirm whether this perspective is consistent across the industry.

Accordingly, the motivation behind starting a seaweed business often aligns with fulfilling some of the UN’s SDGs, such as SDG6 (Clean Water and Sanitation), SDG13 (Climate Action), and SDG14 (Life below Water)19,20,21. On the other hand, emphasis on the environmental ___domain may reflect market demand for sustainable products, as customers increasingly seek products with low environmental footprints38, and local communities are concerned about environmental impacts of seaweed aquaculture59.

However, beliefs such as that of P1 that “algae by itself are already a super ecological resource that brings more benefits than consequences.” may limit their proactive pursuit of sustainability. Moreover, generalizations such as “algae have a very positive impact on the marine ecosystem, they attract fish, they attract a lot of aquatic life” (P1) must be taken with care, as the attracted species could also be invasive species or pathogens.

Community Contributions (C3) stood out as a significant theme in the stakeholder interviews with a higher relative frequency of mentionings as compared with statements from the workshop (Fig. 3). Norwegian interviewee N1 stated that “we want it to be a source of income for people who live along the coast… we want to keep it local.” Similarly, N2 pointed out that new seaweed farming jobs could “attract young people who want to settle in the rural areas.”

However, stakeholders understand the link between environmental, cultural, and economic sustainability, as N3 reflected: “However, if large areas in the fjords are to be set aside for kelp cultivation, such as in China, this will mean significant encroachment on the environment, which in turn can create dissatisfaction in the local community”. Similarly, N1 points out that: “there is demand in the market for sustainability in production. This in turn has an impact on sales and price etc.” Thus, prioritizing environmental sustainability not only protects biodiversity but also facilitates economic sustainability of the seaweed industry through social acceptance.

Production costs (Ec3) were a significant concern for Norwegian stakeholders (Fig. 3). N1 noted, ”The cost of production is so high that the market is very small”. Similarly, N3 stated: “For us as growers, it is not profitable as of today. The cost level of equipment and labor comes into play here.” N1 stated, “Wet biomass is sold for approx. NOK 25 per kg… we need to drop to NOK 15–20 per kg of wet mass, in order for there to be greater demand.“ In addition to lower labor costs in Portugal, Portuguese seaweed fetches higher market prices (green algae such as Ulva and Codium, averaging 0.79 USD/kg, and red algae such as Porphyra and Gracilaria priced at 0.89 and 0.54 USD/kg respectively) than Norwegian kelp (Saccharina, priced at 0.37 USD/kg)4,9. Therefore, Portuguese seaweed has a higher wholesale price of 1350–10,090 USD per ton, making it more profitable than Norwegian seaweed, which has a price between 880 and 980 USD per ton (https://www.selinawamucii.com/).

Enquiry and learning (C1) played a larger role in interviews with Portuguese than with Norwegian stakeholders (Fig. 3), for two likely reasons: 1) In Portugal, seaweed farmers appear to be less aware of environmental risks: “I honestly don’t see any major negative effects that this production has… on the contrary, I think that the production of macroalgae, whether on land or at sea, can mitigate other environmental problems” (P3). This certainly results from the lack of research in this field, and the positive effects of small-scale farms on benthic and pelagic fauna17 as well as on ecosystem services60. 2) Other Portuguese interviewees, such as P1, reported acts of sabotage on seaweed farms: “… fishers who depend on fishing suddenly see here algae cultivation and can see their profession put at risk and there are examples of several companies that test to produce macroalgae and then they see that the buoys were sabotaged, or the ropes were cut by fishers who felt threatened by this innovation”. These tensions highlight that coastal marine businesses need to be re-assured that seaweed farming can be more of a chance than a threat to their profession, and the need for awareness training to promote cooperation and to monitor sustainability thresholds. Since seaweed farming and fishing seasons do not overlap, they could indeed provide full-term employment for seasonal workers, fostering synergies between industries61.

Seven steps in a roadmap towards a sustainable European seaweed industry

The sustainable development of the seaweed industry has been widely discussed62,63,64, yet our results contribute a data-driven roadmap grounded in stakeholder interviews and a workshop, with a focus on actions that satisfy multiple sustainability dimensions—economic, ecological, societal, and governance—at once. The roadmap steps can either be market-pulled by customer needs and regulations, or market-pushed by new technologies that are not yet in demand. By filtering only for actions that address at least two sustainability goals (Supplementary Fig. 6, Supplementary Data 3), this proposed roadmap offers a pathway that integrates multiple sustainability dimensions, ensuring that the industry develops holistically, and facilitates cross-disciplinary collaboration with mutual benefits to both industry and academia.

By grouping the proposed actions that bridge the gap between the future vision for a sustainable seaweed industry and the current situation (Fig. 2), we identified seven overarching roadmap topics in our workshop (Supplementary Data 1). These topics are: 1) Boundaries for carrying capacity, 2) Awareness and education, 3) Multidisciplinary collaboration, 4) Regulations, 5) Research focus, 6) Ecosystem with benefits in multiple areas, 7) Market and product development.

Our SWOT analysis of the workshop revealed 168 statements—23 Strengths, 37 Weaknesses, 46 Opportunities, and 62 Threats—38 of which contributed to synergistic sustainability across multiple dimensions. These insights directly informed the seven roadmap steps. Boundaries for carrying capacity addresses threats from insufficient research on large-scale impacts and the assumption that small-scale benefits scale up, as well as weaknesses in limited understanding of environmental impacts. Awareness and education addresses weak public understanding and threats of community resistance due to perceived environmental and aesthetic impacts, while seizing opportunities to increase acceptance through knowledge sharing. Multidisciplinary collaboration builds on strong research–industry ties and seizes opportunities for cross-sector synergies, while mitigating threats from the lack of coordinated stakeholder involvement. Regulations addresses weaknesses in regulations poorly adapted to seaweed farming, and threats from unregulated rapid growth. Research focus responds to knowledge gaps in large-scale seaweed farming’s environmental effects, and draws from the strong industry–research partnerships for advancement in biotechnology and ecological understanding. Ecosystem services highlights the opportunity to replace more harmful industries, while avoiding the threat of overstating carbon sequestration potential. Market and product development targets weaknesses in public awareness and regulatory delays, addressing threats from consumer skepticism and unlocking opportunities through culturally relevant, high-value products.

Setting boundaries for carrying capacity

The first roadmap step focused on area usage, biomass production, and carbon footprint. Establishing research-based thresholds is crucial to prevent potential social and ecological consequences64, such as dependence on fertilizers65 or hampering of phytoplankton production66. Some farmers, such as N1 underestimate the impacts of upscaling: “Research results show that the environmental consequences of production are minimal, at least to the extent we have today, but we do not think that will change with increased production”. Others, such as N2 recognize: “…we must know what we are doing before we consider scaling up production. We want to avoid making the same mistakes that have been made in other types of food production, both on land and at sea, resulting in problems with large-scale monoculture farming. Everything from alien species, disease, and reduced biological diversity”. Monitoring is essential to track how close the industry moves along identified thresholds, but clear guidelines are lacking24,67,68. Both monitoring needs to detect 1) poorly predictable impacts18 and 2) targeted high-risk aspects28,69 are met by extensively assessing the ecological state before establishing a farm–ideally state-subsidized, followed with site-specific targeted monitoring at defined intervals. Environmental DNA (eDNA) monitoring70 could help with targeted monitoring of high-risk factors like invasive species, endangered species, and pathogens28. Collaboration among biologists, entrepreneurs, and data scientists is needed to develop standard monitoring programs. Mitigation strategies, such as moving large-scale farms offshore and sourcing reproductive material only locally, can reduce risks, like farm shading, competition for space, and genetic homogenization. By selecting at least 100 parent seaweeds, farms can preserve genetic diversity71. Thus, mitigation strategies can render monitoring of these particular risks redundant28. Defined thresholds and consideration of unknown consequences must influence seaweed aquaculture growth and expansion when compromising sustainable value creation (Fig. 4).

Conceptual synthesis showing how implementation of the seven roadmap steps contributes to added value in the seaweed industry while staying within ecological production limits. The diagram illustrates that increasing the number of implemented roadmap steps enhances value creation through innovation, ecosystem services, and societal integration. However, expansion of seaweed farming area or biomass production must remain within boundaries defined by sustainability thresholds to avoid trade-offs. The lines represent pathways taking an increasing number of roadmap steps into account along the continuum from volume-focused (bottom) to value-focused (top).

Increasing social acceptance through research-backed education

Roadmap step 2 focuses on awareness and addressing misinformation about the value and risks of seaweed farming through transparency. As consumer demand for environmentally and socially sustainable products grows38, large-scale farming is not readily accepted in coastal communities36,72. Accordingly, our SWOT analysis revealed 21 Threats and 4 Weaknesses spanning across at least 2 sustainability dimensions related to the uncertain environmental impact (Supplementary Data 4, Supplementary Fig. 5).

Fostering social acceptance beyond environmental concerns also requires to proactively engage with local communities. Establishing an early dialgue helps to address social tensions and enables to integrate seaweed farming into existing traditions through transparent spatial planning and participatory decision-making with tranditional users. Thereby, Global G.A.P. certification can enhance trust between farmers and communities36 and, thus, prevent not-in-my-backyard issues. Complementary approaches that link seaweed farming with ecotourism and regenerative aquaculture, can strengthen communities and diversify economies. Moreover, public-private partnerships, and targeted funding mechanisms that incentivize sustainable practices can help to enrure hat economic and environmental benefits align with btoh local interests and long-term viability of the industry. The impact of larger farms and food security risks must be communicated honestly, and contextualized with less sustainable alternative solutions, such as soy as a vegetarian protein source.

Education plays a key role in increasing social approval28,64, extending beyond mere operational acceptance to promoting seaweed products. Lifelong learning, cooking, medical, and cosmetics seminars, and school projects can integrate seaweed into European culture, improving long-term social acceptance73. Recognizing the cultural significance of the coastline and ensuring that developments align with local values will be crucial in positioning the industry as a positive economic force while respecting local identities, traditions, and existing maritime economies.

Building industry synergies and collaborating across disciplines

Roadmap step 3 focuses on establishing synergistic connections. The European seaweed industry should seize shared resources and infrastructure with established industries to establish regional industrial symbiosis networks74, and support a circular economy. Opportunities of the marine spatial planning approach to boost seaweed aquaculture include integrating seaweed farming with IMTA aquaculture systems, and wind farms75,76,77,78, and tourism. For example, the world’s largest IMTA system in Sanggou Bay, China integrates kelp farming with shellfish (e.g., scallops) and sea cucumbers, which recycle organic waste and improve water quality79. This approach has been shown to raise economic benefits by 67% when compared with kelp monoculture, and by 92% when compared with scallop monoculture while reducing nutrient loading compared to monoculture farming80.

Offshore seaweed farms could co-use the infrastructure of wind energy parks and, in turn, attract fish to those parks. Furthermore, developing mobile and lightweight gear can provide yearly employment to seasonal workers in the fishing and aquaculture industries61. Excess industrial heat could fuel seaweed drying. A largely unexplored potential that corresponds with the strategic guidelines for integrating suitable aquaculture activities into protected areas for the sustainable development of the EU aquaculture5 lies in combining farming with restoration. Here, Saccharina latissima (Phaeophyceae) hatcheries and farms could provide refugia for these endangered habitat types81,82, facilitating large-scale seeding on rocks or biodegradable culturing ropes83. Collaboration between producers and researchers will advance sustainable growth through innovation and improved decision-making (84,85, fostering multinational partnerships across Europe.

Establishing industry-specific regulations that protect diversity

Roadmap step 4 focuses on tailoring regulations to the seaweed industry. Rigidly applying finfish aquaculture regulations to seaweed cultivation has hindered the growth of the seaweed market. Legislation supporting the seaweed industry must focus on diversity at the genetic, species, regional, and stakeholder levels. Low genetic diversity has hampered the production of Asian kelp cultures, as in the case of Undaria pinnatifida (Phaeophyceae)71. Maintaining genetic diversity requires strategies like 1) preventing interbreeding between farmed and wild seaweeds, 2) sourcing spores locally, and 3) storing local and national genetic variants as seed banks (Hu et al., 2024). Although initiatives in this direction have begun, they require global coordination86. Species diversity refers to the ability to adjust regulations to the different taxa cultivated, and the need to link historically eaten seaweed to their current names to ensure that they are still recognized as edible. Food safety should focus on contaminants, such as heavy metals, prometryn, and radionuclide substances87,88,89 rather than taxonomic names. Regional diversity labels should track seaweed origin, preventing cheaper imports from diminishing local production. For example, prohibiting drying seaweed outdoors in Norway but not in Asia raises the costs of European biomass beyond the import price. Stakeholder diversity facilitates coastal small-scale family businesses to co-exist with larger offshore farms around wind parks. This further balances the use of coastal marine space with existing industries.

Conducting research to document impact and facilitate innovation

Roadmap step 5 emphasizes research to assess environmental impacts, map genetic connectivity, advance seaweed biotechnology and ecosystem services. Asia’s long history of seaweed farming offers a unique opportunity to identify the ecological effects of large-scale cultivation90,91, and how farmed cultivars interact with wild populations31 Research at the crossroads of technology and biology can instrumentalize labor-intensive tasks, such as deployment and harvesting15,28,92. Moreover, technological innovations, like AI-based video monitoring can benefit not only the European seaweed industry but also global partnerships. Biotechnology research has the potential to secure production in the context of unpredictable environmental challenges, such as the 2021–2022 red tide that diminished the kelp harvest in Rongcheng, Shandong (China)93. Breeding fast-growing or pathogen-resistant strains benefits both farming and restoration, and if sterile, does not risk admixture with wild populations but often requires replenishing genetic variation to prevent productivity from decreasing71,90,94. Additionally, modern approaches, like microbiome engineering, and priming-induced epigenetic programming94,95, which already strengthen crop plants96,97,98,99,100, must be adapted to algae aquaculture systems95. At the same time, characterizing pathogens and diseases, and understanding how seaweeds defends themselves against these diseases are key to farm production in the future.

Valorizing ecosystem services

Roadmap step 6 revolves around retaining the value of coastal regions through localized licensing, and solutions for the economic sustainability of smaller family businesses. Seaweed farming contributes to the United Nations Sustainable Development Goals20,60, including SDG2 (Zero Hunger), and SDG3 (Good Health and Well-being), by addressing nutritional deficiencies in modern-day human diets101. Moreover, seaweed farms provide ecosystem services that add to the total economic value102, as they can bioremediate waste water, enhance biodiversity and health of marine environments103,104,105,106, and provide biological pest control through oxygenation and biocidal properties107,108,109. Valued at 65,000 Euros/ha/yr110, the bioremediation potential of 35.7 billion tons of global seaweed production2 represents 26% of its commercial value (1.2-3.5 billion USD)111. However, promoting seaweed farming as a significant carbon storage solution is misleading. For example, stakeholder P1 mentioned “In addition to selling algae, one of our main goals is the absorption of carbon dioxide from the environment…”, and “Algae absorb 3–10 times more carbon dioxide from the environment than terrestrial plants. Therefore, these services alone I think are going to be a booster of the seaweed industry”. For seaweed biomass to effectively store carbon for more than 50 years, it must sink to the deep sea, which is neither ecologically nor economically sustainable112. Even if all currently farmed algae sink to the deep sea, they would sequester only 2 million tons of CO2, which is 1% of what the world’s wild kelp forests sequester113, and only approximately 0.005% of the global CO2 emissions in 2022 (37.8 Gt)114. At a rate of approximately 32 Euros/ha/yr for carbon removal, carbon credits for the total global seaweed production amount to only 26.5 million Euros63. Instead, seaweed farming is better positioned as a source of carbon-neutral food production, and an alternative to synthetic soil fertilizers that emit CO2113,115.

Developing a seaweed-based market

Roadmap step 7 targets developing products that resonate with European culture and society while ensuring local value creation, including advanced seeding technologies, circular economy approaches, and the marketing of ecosystem services and diverse products. Although interest in algae-based products is growing, Europe struggles to make seaweed farming economically viable116. A market that values sustainable production and regional authenticity can command higher prices117,118,119. Certifications, such as protected geographical indications (PGI and PDO) and the Norwegian ‘SeaGreens of Norway’, and traceability systems120 can justify the higher price of locally produced seaweed as compared with Asian imports. Incorporating seaweed into traditional foods, such as the Dutch wheat burger, pasta, ravioli, or seaweed sausage119, can further increase demand. Trends, such as the ‘New Nordic Cuisine,’ emphasizing local and natural foods, and the ‘superfood’ trend, advocating nutrient-dense foods, can help make seaweed a regular part of European diets121.

Economic sustainability on the European market relies on a kg fresh weight (FW) price of approximately 1 Euro (approximately 6700 Euros per ton dry weight (DW), assuming 15% DW), to exceed the estimated production costs that range from 1800 to 5200 per ton DW35,122,123. This requires an established market of high-value products122, such as fertilizer, biostimulants, biopesticides, biochar, nutraceuticals, and pharmaceuticals111,119. Europe can follow the lead of China, which has developed kelp-based innovative industrial clusters, such as alginates, functional food (e.g., jelly, drink, and pet food), sugar alcohol (e.g., mannitol and sorbitol), cosmetics (e.g., mask, wash, and care), medical materials (e.g., fiber and chemicals), and fertilizer. Therefore, a network of collaborators such as farmers, suppliers, universities, and customers increases the chances of innovative and successful products in the market124,125.

Conclusions

The European seaweed industry has the unique opportunity to distinguish itself as an industry that prioritizes sustainability alongside economic growth. The European Commission supports sustainable growth in seaweed farming through funding opportunities in the European Maritime, Fisheries and Aquaculture Fund (EMFAF) and Horizon Europe for algae-related research and innovation.

Insights from part of the Norwegian and Portuguese industries, representing the latitudinal extremes of the European seaweed industry, show contrasting yet complementary strengths and strategies. While personal communication with a broader range of stakeholders aligned with these insights, we did not include other European countries with seaweed farming in our interviews or workshop.

Expanding our research through questionnaires focusing on our roadmap steps, and including stakeholders from additional regions would allow us to better characterize differences in sustainable practices and industry visions across Europe. This would allow us to direct research partnerships based on how sustainable practices and visions vary, and where roadmap elements are already practiced or should be strengthened across Europe.

Our roadmap offers a pathway for researchers, policymakers, communities, and industry stakeholders as Phase III to implement sustainable practices in the European seaweed industry47. To reach Phase IV, which assesses the effectiveness of these actions, we must now implement the proposed roadmap steps that require trust and understanding across disciplines to foster innovation through collaboration among researchers, governments, and businesses. Future research should evaluate how well the roadmap supports sustainable seaweed production by balancing the environmental, economic, and social factors. Long-term studies are necessary to assess the real-world impacts of these sustainable practices.

Data availability

The data analyzed during this study are included in this published article and its supplementary information files, with the exception of raw interview transcripts and complete workshop discussion texts. These contain personal information and were excluded to protect the privacy and anonymity of the participants.

Abbreviations

- ASC:

-

Aquaculture Stewardship Council

- DNA:

-

Desoxyribonucleic acid

- DW:

-

Dry Weight

- eDNA:

-

environmental DNA

- FW:

-

Fresh Weight

- G.A.P:

-

Good Agricultural Practices

- IMTA:

-

Integrated Multi Trophic Aquaculture

- MSC:

-

Marine Stewardship Council

- SDG:

-

Sustainable Development Goal

- SWOT:

-

Strengths, Weaknesses, Opportunities, Threats

- UN:

-

United Nations

- WOS:

-

Wheel of Sustainability

References

Costa-Pierce, B. A. Restorative aquaculture for people, profit and planet. INFOFISH Int. 51, 50–55 (2024).

FAO. FAO Aquaculture News, May 2021 (FAO, 2021).

European Commission. The EU blue economy report 2022 (Publications Office of the European Union, 2022) https://doi.org/10.2771/793264.

Cai, J. Seaweeds and microalgae: an overview for unlocking their potential in global aquaculture development (FAO, 2021) https://doi.org/10.4060/cb5670en.

European Commission. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions (European Commission, 2021) https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM%3A2022%3A230%3AFIN.

Araújo, R. et al. Current Status of the Algae Production Industry in Europe: An Emerging Sector of the Blue Bioeconomy. Front. Mar. Sci. 7, 1–24 (2021).

Havforskningsinstituttet. Havforskningsrapporten 2016. Fisken og havet 3, 08020620 (2016).

Slotsvik, G. N. et al. Norwegian blue forests network (NBFN)-Top ten trends from 2023, GRID-Arendal. Arendal, Norway. https://coilink.org/20.500.12592/70rz2g2 (2024).

Gaspar, R., Pereira, L. & Sousa-Pinto, I. The seaweed resources of Portugal. Botanica Mar. 62, 499–525 (2019).

Kuech, A., Breuer, M. & Popescu, I. Research for PECH committee-the future of the EU algae sector (European Parliament, Policy Department for Structural and Cohesion Policies, 2023).

Hu, Z. et al. Kelp breeding in China: Challenges and opportunities for solutions. Rev. Aquac. 16, 855–871 (2024).

Draisma, M. Study on existing market for algal food applications Part A: Seaweed (Deliverable D4.1.1). North Sea Farm Foundation. https://www.northseafarmers.org/projects/D4.1.1A_Study-on-the-existing-market-for-seaweed-food-applications.pdf (2019).

Coleman, S. et al. Quantifying baseline costs and cataloging potential optimization strategies for kelp aquaculture carbon dioxide removal. Front Mar. Sci. 9, 966304 (2022).

Campbell, I. et al. The Environmental Risks Associated With the Development of Seaweed Farming in Europe - Prioritizing Key Knowledge Gaps. Front Mar. Sci. 6, 107 (2019).

Feehan, C. J. Seaweed Farming: Assessment on the Potential of Sustainable Upscaling for Climate, Communitiesand the Planet. Edited by Jonsson, L. & Blanchard, H. V. United Nations Environment Programme, Nairobi (2023).

Kim, J. K., Yarish, C., Hwang, E. K., Park, M. & Kim, Y. Seaweed aquaculture: Cultivation technologies, challenges and its ecosystem services. Algae 32, 1–13 (2017).

Visch, W., Kononets, M., Hall, P. O. J. J., Nylund, G. M. & Pavia, H. Environmental impact of kelp (Saccharina latissima) aquaculture. Mar. Pollut. Bull. 155, 110962 (2020).

Bekkby, T. et al. ‘Hanging gardens’ — comparing fauna communities in kelp farms and wild kelp forests. Front. mar. sci. 10, 1066101 (2023).

Spillias, S. et al. Expert perceptions of seaweed farming for sustainable development. J. Clean. Prod. 368, 133052 (2022).

Duarte, C. M., Bruhn, A. & Krause-Jensen, D. A seaweed aquaculture imperative to meet global sustainability targets. Nat. Sustain. https://doi.org/10.1038/s41893-021-00773-9 (2021).

Gao, K. & Beardall, J. Using macroalgae to address UN Sustainable Development goals through CO 2 remediation and improvement of the aquaculture environment. Appl. Phycol. 00, 1–8 (2022).

Hossain, M. S. et al. Seaweeds farming for sustainable development goals and blue economy in Bangladesh. Mar. Policy 128, 104469 (2021).

Ktari, L., Chebil Ajjabi, L., De Clerck, O., Gómez Pinchetti, J. L. & Rebours, C. Seaweeds as a promising resource for blue economy development in Tunisia: current state, opportunities, and challenges. J. Appl. Phycol. 34, 489–505 (2022).

Hancke, K. et al. Miljøpåvirkninger av taredyrking og forslag til utvikling av overvåkingsprogram (2021).

Vincent, A., Stanley, A. & Ring, J. Hidden champion of the ocean: Seaweed as a growth engine for a sustainable European future. Seaweed for Europe, 60, https://www.seaweedeurope.com/hidden-champion/ (2020).

Bao, Y. & Xu, P. Implications of Environmental Variations on Saccharina japonica Cultivation in Xiangshan Bay, China. Biology 14, 175 (2025).

Zhang, Y. et al. Adverse Environmental Perturbations May Threaten Kelp Farming Sustainability by Exacerbating Enterobacterales Diseases. Environ. Sci. Technol. 58, 5796–5810 (2024).

Campbell, I. et al. The environmental risks associated with the development of seaweed farming in Europe - prioritizing key knowledge gaps. Front. Marine Sci. 6, https://doi.org/10.3389/fmars.2019.00107 (2019).

Grebe, G. S., Byron, C. J., Gelais, A. S., Kotowicz, D. M. & Olson, T. K. An ecosystem approach to kelp aquaculture in the Americas and Europe. Aquac. Rep. 15, 100215 (2019).

Stévant, P., Rebours, C. & Chapman, A. Seaweed aquaculture in Norway: recent industrial developments and future perspectives. Aquac. Int. 25, 1373–1390 (2017).

Graf, L. et al. A genome-wide investigation of the effect of farming and human-mediated introduction on the ubiquitous seaweed Undaria pinnatifida. Nat. Ecol. Evol. 5, 360–368 (2021).

Zhang, J. et al. Effect of domestication on the genetic diversity and structure of Saccharina japonica populations in China. Sci. Rep. 7, 42158 (2017).

Bhuyan, S. Ecological risks associated with seaweed cultivation and identifying risk minimization approaches. Algal Res. 69, 102967 (2023).

Wood, D., Capuzzo, E., Kirby, D., Mooney-McAuley, K. & Kerrison, P. UK macroalgae aquaculture: What are the key environmental and licensing considerations? Mar. Policy 83, 29–39 (2017).

van den Burg, S. W. K., van Duijn, A. P., Bartelings, H., van Krimpen, M. M. & Poelman, M. The economic feasibility of seaweed production in the North Sea. Aquac. Econ. Manag. 20, 235–252 (2016).

Billing, S.-L., Rostan, J., Tett, P. & Macleod, A. Is social license to operate relevant for seaweed cultivation in Europe? Aquaculture 534, 736203 (2021).

Krause, G. et al. A revolution without people? Closing the people–policy gap in aquaculture development. Aquaculture 447, 44–55 (2015).

Galbreth, M. R. & Ghosh, B. Competition and Sustainability: The Impact of Consumer Awareness: Competition and Sustainability. Decis. Sci. 44, 127–159 (2013).

Odobaša, R. & Marošević, K. Expected contributions of the European Corporate Sustainability Reporting Directive (CSRD) to the sustainable development of the European Union. EU Comp. Law Issues Chall. Ser. 7, 593–612 (2023).

Bagheri, A. & Hjorth, P. Planning for sustainable development: a paradigm shift towards a process‐based approach. Sustain. Dev. 15, 83–96 (2007).

Hardi, P. & Zdan, T. J. Assessing sustainable development: principles in practice (International Institute for Sustainable Development, 1997).

Nilsson, J. & Bergström, S. Indicators for the assessment of ecological and economic consequences of municipal policies for resource use. Ecol. Econ. 14, 175–184 (1995).

Nonaka, I. & Toyama, R. The theory of the knowledge-creating firm: subjectivity, objectivity and synthesis. Ind. Corp. Change 14, 419–436 (2005).

Voss, J.-P. & Kemp, R. Reflexive Governance: Learning to cope with fundamental limitations in steering sustainable development. Futures 39, 275–302 (2005).

Davis, A. & Sharp, J. Rethinking One Health: Emergent human, animal and environmental assemblages. Soc. Sci. Med. 258, 113093 (2020).

Executive Agency for Small and Medium sized Enterprises, Technopolis Group., Wageningen Research. Blue Bioeconomy Forum: roadmap for the blue bioeconomy (Publications Office, 2020) https://doi.org/10.2826/605949. Accessed 19 Aug 2023.

De Ridder, W., Turnpenny, J., Nilsson, M. & Von Raggamby, A. A framework for tool selection and use in integrated assessment for sustainable development. J. Environ. Assessment Policy Manag. 9, 423–441 (2007).

Huang, R. RQDA: R-based Qualitative Data Analysis. R package version 0.2-8. http://rqda.r-forge.r-project.org/ (2016).

Bishop, P., Hines, A. & Collins, T. The current state of scenario development: an overview of techniques, https://doi.org/10.1108/14636680710727516 (2007).

Okada, Y., Kishita, Y., Nomaguchi, Y., Yano, T. & Ohtomi, K. Backcasting-Based Method for Designing Roadmaps to Achieve a Sustainable Future. IEEE Trans. Eng. Manag. 69, 168–178 (2022).

Osmundsen, T. C. et al. The operationalisation of sustainability: Sustainable aquaculture production as defined by certification schemes. Global Environ. Change 60, https://doi.org/10.1016/j.gloenvcha.2019.102025 (2020).

James, P., Magee, L., Scerri, A. & Steger, M. Urban sustainability in theory and practice: Circles of sustainability, https://doi.org/10.4324/9781315765747 (2014).

Godal, M. S. Operationalisation of sustainability of the Norwegian macroalgae aquaculture industry. Master’s thesis, NTNU, Norway (2020).

Aquaculture Stewardship Council, 2022. Joint standard for environmentallysustainable and socially responsible seaweed production. https://www.ascaqua.org/what-we-do/ourstandards/seaweed-standard/.

Glenn, J. C. The Futures Wheel. In Futures Research Methodology - Version 3.0, edited by Glenn, J. C. & Gordon, T. J. (Washington, DC: Millennium Project, 2009).

Brunson, J. ggalluvial: Layered Grammar for Alluvial Plots. JOSS 5, 2017 (2020).

Cerca, M., Sosa, A. & Murphy, F. Responsible supply systems for macroalgae: Upscaling seaweed cultivation in Ireland. Aquaculture 563, 738996 (2023).

Bjørkan, M. & Billing, S.-L. Commercial Seaweed Cultivation in Scotland and the Social Pillar of Sustainability: A Q-Method Approach to Characterizing Key Stakeholder Perspectives. Front Sustain Food Syst. 6, 795024 (2022).

Larsen, I. 40 innsigelser mot tablering av algeanlegg. Lokalavisa (2022).

Hasselström, L. et al. The impact of seaweed cultivation on ecosystem services - a case study from the west coast of Sweden. Mar. Pollut. Bull. 133, 53–64 (2018).

St-Gelais, A. T. et al. Engineering A Low-Cost Kelp Aquaculture System for Community-Scale Seaweed Farming at Nearshore Exposed Sites via User-Focused Design Process. Front. Sustain. Food Syst. 6, https://doi.org/10.3389/fsufs.2022.848035 (2022).

Barbier, M., Araújo, R., Rebours, C., Jacquemin, B., Holdt, S. L. & Charrier, B. Development and objectives of the PHYCOMORPH European Guidelines for the Sustainable Aquaculture of Seaweeds (PEGASUS). Botanica Mar. 63, 5–16 (2020).

Costa-Pierce, B. A. & Chopin, T. The Hype, Fantasies and Realities of Aquaculture Development Globally and In Its New Geographies (World Aquaculture, 2021).

Cottier-Cook, E. J. et al. Ensuring the sustainable futureof the rapidly expanding global seaweed aquaculture industry – a vision. United Nations University Instituteon Comparative Regional Integration Studies and Scottish Association for Marine Science Policy Brief (2021).

Fan, W. et al. Nutrient Removal from Chinese Coastal Waters by Large-Scale Seaweed Aquaculture Using Artificial Upwelling. Water 11, 1754 (2019).

Shi, J. et al. A physical–biological coupled aquaculture model for a suspended aquaculture area of China. Aquaculture 318, 412–424 (2011).

Bārda, I. et al. Ensuring environmental safety–necessary monitoring practices for seaweed cultivation andharvesting in the Baltic Sea. Report for the “Safe Seaweed Coalition” project “BalticSeaSafe”, Deliverable O.1 (2022).

Norderhaug, K. M., Hansen, P. K., Fredriksen, S., Grøsvik, B. E. & Naustvoll, J. Miljøpåvirkning fra dyrking avmakroalger—Risikovurdering for norske farvann. Report fo the institute of Marine Research, Norway (2021).

Wilding, T. A. et al. Turning off the DRIP (‘Data-rich, information-poor’) – rationalising monitoring with a focus on marine renewable energy developments and the benthos. Renew. Sustain. Energy Rev. 74, 848–859 (2017).

Lynn, J. S., Klanderud, K., Telford, R. J., Goldberg, D. E. & Vandvik, V. Macroecological context predicts species’ responses to climate warming. Glob. Change Biol. 27, 2088–2101 (2021).

Shan, T. F., Pang, S. J., Li, J. & Gao, S. Q. Breeding of an elite cultivar haibao no. 1 of Undaria pinnatifida (phaeophyceae) through gametophyte clone crossing and consecutive selection. J. Appl. Phycol. 28, 2419–2426 (2016).

Cottier-Cook, E. J. et al. Safeguarding the future of the global seaweed aquaculture industry, 12. United Nations University and Scottish Association for Marine Science Policy Brief. (United Nations University (INWEH) and Scottish Association for Marine Science, 2016).

Cornish, M. L., Critchley, A. T. & Mouritsen, O. G. Consumption of seaweeds and the human brain. J. Appl Phycol. 29, 2377–2398 (2017).

Giannoccaro, I., Zaza, V. & Fraccascia, L. Designing regional industrial symbiosis networks: The case of Apulia region. Sustain. Dev. 31, 1475–1514 (2023).

Gimpel, A. et al. A GIS modelling framework to evaluate marine spatial planning scenarios: Co-___location of offshore wind farms and aquaculture in the German EEZ. Mar. Policy 55, 102–115 (2015).

United Nations Environment Programme NBFN. Into the Blue: Securing a Sustainable Future for Kelp Forests (United Nations Environment Programme NBFN, 2023) https://wedocs.unep.org/20.500.11822/42255.

Buck, B. H. et al. State of the Art and Challenges for Offshore Integrated Multi-Trophic Aquaculture (IMTA). Front. Mar. Sci. 5, 165 (2018).

Le Gouvello, R. et al. Aquaculture and marine protected areas: Potential opportunities and synergies. Aquat. Conserv. Mar. Freshw. Ecosyst. 27, 138–150 (2017).

Fang, J., Zhang, J., Xiao, T., Huang, D. & Liu, S. Integrated multi-trophic aquaculture (IMTA) in Sanggou Bay, China. Aquac. Environ. Interact. 8, 201–205 (2016).

Shi, H., Zheng, W., Zhang, X., Zhu, M. & Ding, D. Ecological–economic assessment of monoculture and integrated multi-trophic aquaculture in Sanggou Bay of China. Aquaculture 410–411, 172–178 (2013).

Gundersen, H., Bekkby, T., Norderhaug, K. M., Oug, E., Rinde, E. & Fredriksen, S. Sukkertareskog i Nordsjøen og Skagerrak, Marint gruntvann. https://artsdatabanken.no/RLN2018/342 (2018).

Gundersen, H. et al. Sukkertareskog i Norskehavet og Barentshavet, Marint gruntvann. Norsk rødliste for naturtyper 2018. https://artsdatabanken.no/RLN2018/342 (2018).

Filbee-Dexter, K. et al. Leveraging the blue economy to transform marine forest restoration. J. Phycol. 58, 198–207 (2022).

Mezirow, J. Learning as Transformation: Critical Perspectives on a Theory in Progress. The Jossey-Bass Higher and Adult Education Series (Jossey-Bass Publishers, 2000).

Iñigo, E. A. & Albareda, L. Understanding sustainable innovation as a complex adaptive system: a systemic approach to the firm. J. Clean. Prod. 126, 1–20 (2016).

Wade, R. et al. Macroalgal germplasm banking for conservation, food security, and industry. PLoS Biol. 18, 1–10 (2020).

Duarte, B. et al. Fatty acid profiles of estuarine macroalgae are biomarkers of anthropogenic pressures: Development and application of a multivariate pressure index. Sci. Total Environ. 788, 147817 (2021).

Mendes, M. et al. Algae as Food in Europe: An Overview of Species Diversity and Their Application. Foods 11, 1871 (2022).

Yoshida, N. & Kanda, J. Tracking the Fukushima Radionuclides. Science 336, 1115–1116 (2012).

Hu, Z. et al. Kelp aquaculture in China: a retrospective and future prospects. Rev. Aquaculture, https://doi.org/10.1111/raq.12524 (2021).

Hurtado, A. Q., Neish, I. C. & Critchley, A. T. Phyconomy: the extensive cultivation of seaweeds, their sustainability and economic value, with particular reference to important lessons to be learned and transferred from the practice of eucheumatoid farming. Phycologia 58, 472–483 (2019).

Solvang, T., Bale, E. S., Broch, O. J., Handå, A. & Alver, M. O. Automation Concepts for Industrial-Scale Production of Seaweed. Front. Mar. Sci. 8, 613093 (2021).

Li, X. Comprehensive Analysis of Large-Scale Saccharina japonica Damage in the Principal Farming Area of Rongcheng in Shandong Province from 2021 to 2022. https://www.nkdb.net/EN/10.13304/j.nykjdb.2022.0728 (2023). Accessed 17 Sep 2023.

Hu, Z.-M. Kelp breeding in China: Challenges and opportunities for solutions. Rev. Aquaculture, https://doi.org/10.1111/raq.12871 (2023).

Jueterbock, A. et al. Priming of Marine Macrophytes for Enhanced Restoration Success and Food Security in Future Oceans. Front. Mar. Sci. 8, 279 (2021).

Afridi, M. S. et al. New opportunities in plant microbiome engineering for increasing agricultural sustainability under stressful conditions. Front Plant Sci. 13, 899464 (2022).

Hilker, M. et al. Priming and memory of stress responses in organisms lacking a nervous system. Biol. Rev. 91, 1118–1133 (2016).

Morales Moreira, Z. P., Chen, M. Y., Yanez Ortuno, D. L. & Haney, C. H. Engineering plant microbiomes by integrating eco-evolutionary principles into current strategies. Curr. Opin. Plant Biol. 71, 102316 (2023).

Pawar, V. A. & Laware, S. L. Seed priming a critical review. Int. J. Sci. Res. Biol. Sci. 5, 94–101 (2018).

Wojtyla, Ł., Lechowska, K., Kubala, S. & Garnczarska, M. Molecular processes induced in primed seeds—increasing the potential to stabilize crop yields under drought conditions. J. Plant Physiol. 203, 116–126 (2016).

Holdt, S. L., Kraan, S. & Kraan, S. Bioactive compounds in seaweed: functional food applications and legislation. J. Appl. Phycol. 23, 543–597 (2011).

United Nations Environment Programme, Djampou A, Norwegian Blue Forests Network. Into the Blue: Securing a Sustainable Future for Kelp Forests. United Nations Environment Programme, https://doi.org/10.59117/20.500.11822/42255 (2023).

Beheshti, K. et al. Rapid enhancement of multiple ecosystem services following the restoration of a coastal foundation species. Ecological Appl. https://doi.org/10.1002/eap.2466 (2021).

Williams, C. et al. Rewilding the Sea? A Rapid, Low Cost Model for Valuing the Ecosystem Service Benefits of Kelp Forest Recovery Based on Existing Valuations and Benefit Transfers. Front. Ecol. Evol. 10, https://doi.org/10.3389/fevo.2022.642775 (2022).

Forbes, H., Shelamoff, V., Visch, W., Layton, C. & Forbes, H. Farms and forests: evaluating the biodiversity benefits of kelp aquaculture. J. Appl. Phycol. https://doi.org/10.1007/s10811-022-02822-y (2022).

Theuerkauf, S. J. et al. Habitat value of bivalve shellfish and seaweed aquaculture for fish and invertebrates: Pathways, synthesis and next steps. Rev. Aquaculture, https://doi.org/10.1111/raq.12584 (2021).

Echave, J. et al. Seaweed-Derived Proteins and Peptides: Promising Marine Bioactives. Antioxidants 11, https://doi.org/10.3390/antiox11010176 (2022).

Vicente, T. F. L., Félix, C., Félix, R., Valentão, P. & Lemos, M. Seaweed as a Natural Source against Phytopathogenic Bacteria. Marine Drugs, https://doi.org/10.3390/md21010023 (2022).

Vicente, T. F. L. et al. Marine Macroalgae, a Source of Natural Inhibitors of Fungal Phytopathogens. J. Fungi 7, 1006 (2021).

Eger, A. et al. The economic value of fisheries, blue carbon, and nutrient cycling in global marine forests. EcoEvoRxiv. https://doi.org/10.32942/osf.io/n7kjs (2021).

Chopin, T. & Tacon, A. G. J. Importance of Seaweeds and Extractive Species in Global Aquaculture Production. Rev. Fish. Sci. Aquac. 29, 139–148 (2021).

Chopin, T. et al. Deep-ocean seaweed dumping for carbon sequestration: Questionable, risky, and not the best use of valuable biomass. One Earth 7, 359–364 (2024).

Duarte, C. M., Wu, J., Xiao, X., Bruhn, A. & Krause-Jensen, D. Can seaweed farming play a role in climate change mitigation and adaptation? Front. Marine Sci. 4, https://doi.org/10.3389/fmars.2017.00100 (2017).

European Commission. Joint Research Centre. CO2 emissions of all world countries: JRC/IEA/PBL 2022 report (Publications Office: LU, 2022) https://doi.org/10.2760/730164. Accessed 1 Aug 2023.

Nabti, E., Jha, B., Jha, B., Hartmann, A., Hartmann, A. & Hartmann, A. Impact of seaweeds on agricultural crop production as biofertilizer. Int. J. Environ. Sci. Technol. 14, 1119–1134 (2017).

Stévant, P. & Rebours, C. Landing facilities for processing of cultivated seaweed biomass: a Norwegian perspective with strategic considerations for the European seaweed industry. J. Appl. Phycol. 33, 3199–3214 (2021).

Brayden, W. C., Noblet, C. L., Evans, K. S. & Rickard, L. Consumer preferences for seafood attributes of wild-harvested and farm-raised products. Aquac. Econ. Manag. 22, 362–382 (2018).

Dagevos, H. & Van Ophem, J. Food consumption value: Developing a consumer-centred concept of value in the field of food. Br. Food J. 115, 1473–1486 (2013).

Van Den Burg, S. W. K., Dagevos, H. & Helmes, R. J. K. Towards sustainable European seaweed value chains: a triple P perspective. ICES J. Mar. Sci. 78, 443–450 (2021).

Duarte, B., Mamede, R. & Caçador, I., Melo, R., Fonseca, V. F. Trust your seaweeds: Fine-scale multi-elemental traceability of edible seaweed species harvested within an estuarine system. Algal Res. https://doi.org/10.1016/j.algal.2023.102975 (2023).

Blikra, M. J. et al. Seaweed products for the future: Using current tools to develop a sustainable food industry. Trends Food Sci. Technol. 118, 765–776 (2021).

DeAngelo, J. et al. Economic and biophysical limits to seaweed farming for climate change mitigation. Nat. Plants 9, 45–57 (2022).

LEI International Policy, Van Den Burg, S., Wakenge, C. & Berkhout, P. Economic prospects for large-scale seaweed cultivation in the North Sea (Wageningen Economic Research: Wageningen, 2019) https://doi.org/10.18174/470257.

Baum, J. A. C., Calabrese, T. & Silverman, B. S. Don’t go it alone: alliance network composition and startups’ performance in Canadian biotechnology. Strat. Manag. J. 21, 267–294 (2000).

Faems, D. & Looy, B. Interorganizational Collaboration and Innovation: Toward a Portfolio Approach*. J. Prod. Innov. Manag. 22, 238–250 (2005).

DNV. Oceans’ future to 2050: marine aquaculture forecast. https://www.dnv.com/focus-areas/offshore-aquaculture/marine-aquaculture-forecast/#:~:text=Marine%20aquaculture%20will%20more%20than,weight%20to%2074%20Mt%2Fyr (2021).

Fortune Business Insights. Market Research Report. The global commercial seaweed market is projected to grow from $15.01 billion in 2021 to $24.92 billion in 2028 at a CAGR of 7.51% during forecast period… Read More at:- https://www.fortunebusinessinsights.com/industry-reports/commercial-seaweed-market-100077 (2021).

Acknowledgements

We acknowledge Grete Thuv Tjønndal and Miguel Fernandes for conducting the interviews with stakeholders of the seaweed industry in Norway and Portugal, respectively. This work was supported by the Fund for Bilateral Relations Open Call#1 EEA Financial Mechanism 2014-2021 - iSea project (FBR_OC1_98), and by Nord University (Economic Research). We further acknowledge support from FCT Fundação para a Ciência e a Tecnologia to MARE (https://doi.org/10.54499/UIDB/04292/2020) and (https://doi.org/10.54499/UIDP/04292/2020) and ARNET (https://doi.org/10.54499/LA/P/0069/2020). The funders were not involved in the study design, collection, analysis, and interpretation of data, in the writing of the report, or in the decision to submit the article for publication.

Funding

Open access funding provided by Nord University.

Author information

Authors and Affiliations

Contributions

A.J. and B.D. conceptualized the project, secured funding, and oversaw its execution. Both developed methodologies, and managed resources, with significant contributions from H.H.-H. and K.W. in data curation, methodology refinement, and validation. A.J. additionally took the lead in formal analysis and visualization, shaping the project’s scientific direction. The development of the roadmap was a team effort, with A.C., A.E., A.K., A.M., A.M.L.N., C.B., C.G., G.H., H.M., H.R., L.O., R.M., and R.R. and all contributing significantly with their knowledge and ideas. R.M. additionally contributed to refining the methodology and managing resources. The manuscript, initially drafted by A.J., was shaped by the critical review and edits of A.E., B.D., C.B., D.L.D., H.R., H.H.-H., J.Z., K.W., P.K., R.M., R.R., and Z.M.H. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Jueterbock, A., Hoarau-Heemstra, H., Wigger, K. et al. Roadmap to sustainably develop the European seaweed industry. npj Ocean Sustain 4, 22 (2025). https://doi.org/10.1038/s44183-025-00122-9

Received:

Accepted:

Published:

DOI: https://doi.org/10.1038/s44183-025-00122-9