Abstract

Burning the reserves of the 200 largest fossil fuel companies could generate 673 gigatonnes of carbon dioxide, far exceeding the remaining 400-gigatonne budget needed to limit warming to 1.5 °C by 2050. Rapid action is needed to reduce, or where necessary, offset emissions from burning fossil fuels but it remains unclear who will bear the cost. Our study aims to show the limits of offsetting using reserve data from the 200 largest fossil fuel companies sourced from Fossil Free Funds and carbon capture rates from peer-reviewed ecological studies. We show that if the cost of offsetting fossil fuel emissions exceeds $150 per tonne of carbon dioxide, fossil fuel companies could have negative market valuations. Using the social cost of carbon, we find the climate-related externalities associated with these reserves exceed their market valuation. Afforestation is often proposed as a carbon sequestration solution, but offsetting emissions from fossil fuel reserves would require covering an area the size of North and Central America solely with trees, displacing communities, farmland and existing habitats. Afforestation, while more economical could disrupt existing ecosystems that provide vital ecosystem services.

Similar content being viewed by others

Introduction

Fossil fuel companies own vast fossil reserves. The burning of fossil fuel accounts for 94% of global fuel emissions (cement and other industry uses make up the rest) and the burning of fossil fuel represents 89.6% of global emissions1. In recent communications, fossil fuel companies have started to mention offsetting emissions from their activities. Shell, for example, plans to “offset emissions of around 120 million tonnes a year by 2030”2,3. Carbon offsetting could potentially compensate for carbon emissions, yet the topic is debated4,5,6,7,8,9. We asked two questions: Is carbon offsetting economically viable? How much space is needed for afforestation to compensate for carbon emissions?

This article focusses on the 200 largest holders of fossil fuel reserves. Looking at their reserves today, we calculated the cost and land surface needed for offsetting carbon emissions from burning all their current reserves. Fossil fuel companies currently hold 182 Gt of carbon (equivalent to 673 Gt of CO2e) in their reserves, as reported by Fossil Free Funds CU200. These reserves, recorded on their balance sheets as part of their economic value, would release 673 Gt of CO2e if extracted and burned. This far exceeds the 400 Gt CO2e remaining in our carbon budget10,11. It is estimated that 60% of oil and fossil methane gas, and 90% of coal must remain unextracted to keep within a 1.5 °C carbon budget12. But fossil fuel companies currently face little incentive to reduce the extraction and use of fossil fuels, and regulatory measures to limit these activities have been slow to materialise. These companies list their reserves as assets on their balance sheets, which implies an expectation that those reserves will eventually be extracted and used.

Our study takes a global look at the question of fossil fuel offsetting. This has the advantage of giving general answers to the questions posed. The downside of this approach is that we - rely on many simplifying assumptions. These assumptions are laid out in the methods section.

We focus on offsetting in this paper because IPCC scenarios all contain an offsetting or negative emissions element, along with emission reduction. Also, fossil fuel companies have started communicating on offsetting, and this paper asks what it means if they were to take offsetting seriously. We focus on many forms of negative emissions, such as Carbon Capture and Storage (CCS), carbon markets, or offsetting through afforestation. The idea is to understand the limits of negative emissions. This is to show the importance of reducing emissions instead. Our analysis aligns with existing policies, including the IPCC framework, which emphasises the necessity of reducing emissions before considering offsetting. However, the case of fossil fuel companies is unique, as their value of these companies is closely linked to the value of their fossil reserves, making decarbonisation difficult and leading to a risk of stranded assets13,14.

Our paper first looks at the financial viability of an offsetting approach. We show that offsetting is through carbon markets or direct air capture is prohibitively expensive. We then single out afforestation, currently the cheapest offsetting technology. In this paper, afforestation is defined as the deliberate establishment of new forests on land that currently has no tree cover, excluding instances of natural regeneration and agroforestry. In other words, we refer to the intentional creation of forests on previously non-forested land, distinguishing it from natural forest regrowth15. The estimates we use are for natural regeneration of forests and not for agroforestry15. We show that this technology would use more space than was previously thought. In the literature review, we also show that even if policymakers were willing to sacrifice this space for afforestation, there would still be ecological limitations to be taken into account before starting afforestation at the scale needed. We conclude, in line with a large literature, that the best would be not to burn fossil fuel in the first place and simply leave them in the ground. Instead of burning them and then offsetting them.

First, our paper examines the literature on the social cost of carbon. The social cost of carbon computes the marginal cost of the impacts caused by emitting an additional tonne of carbon emissions16,17. It is also at the heart of the Dynamic Integrated model of Climate and the Economy (DICE) models18,19. The method presented here does not offer a social cost of carbon, but rather computes at which social cost of carbon it becomes no longer economically viable for society to operate fossil fuel companies. We find that at the current estimated social cost of carbon, running fossil fuel companies is not economically viable20. That is, if an additional tonne of CO2 costs society around $190, it would not be economically viable to run any of the 200 largest fossil fuel companies. The environmental damage resulting from burning their oil, gas, and coal reserves outweighs the economic value of these assets.

The second literature this paper touches upon is that of stranded assets. This literature is focused on a similar question on the value of fossil fuel companies. Rich countries have more to lose if fossil assets become stranded. They estimate the net present value of future lost profits in the oil and gas sector at $1 trillion13. States highly dependent on oil and gas revenue could see government revenues drop by 51%21. In Latin America and the Caribbean, around 66–81% of proven and unproven reserves (3P) might not be exploitable22. In order to remain within a 1.5 C scenario, 60% of oil and gas reserves would need to remain in the ground and 90% of coal reserves23. Our findings support this view by showing that the social cost of extracting all fossil reserves exceeds the economic value of these reserves. We show that it makes economic sense to leave fossil fuel reserves in the ground.

Finally, our paper explores the literature on the offsetting potential of our planet. This literature focuses largely on offsetting by afforestation, as does our paper. A paper has recently claimed that there is enough space to offset 200 tonnes of carbon24. These estimates usually stay consistent whether using satellite or ground-sourced data. Estimates of the global capture potential are at around 226 Gt25. That would be just more than all fossil fuel reserves of the 200 largest fossil fuel companies. The difference in our approach is that instead of calculating how much space is available, we ask how much space we need. In illustrative maps, we show how much space would be needed to offset historical emissions, and how much space to offset future planned emissions by fossil fuel companies. This is a new contribution to the literature and highlights some of the shortcomings of afforestation as an offsetting solution.

Our paper relies on a series of simplifying assumptions, which allow for broad-reaching conclusions but are also limitations. We outline the broadest assumption here and present it in more detail in the paper. The first is that we focus on reserves of fossil fuel companies, not their emissions. This is a simplification because fossil fuel companies do not directly burn coal, oil, and gas but simply sell it. Yet, we still think this assumption is valid as the future global temperature depends in part on the extraction of these resources.

Second, we focus primarily on afforestation in this paper, acknowledging that this leaves out other critical approaches such as preventing deforestation, restoring forests, and improving forest management. We made this choice because afforestation is the primary method used by most commercial offset solution providers, and it offers a relatively straightforward way to measure offsets. However, we stress that these other forest-based solutions remain central to tackling climate change and should not be overlooked.

Similarly, while this study focuses on afforestation, while other nature-based solutions such as mangrove restoration or peatland conservation are equally important. These were excluded from our calculations for simplification, but should absolutely be considered by policymakers.

In terms of afforestation, we limit our calculations to afforestation by natural regeneration, as defined in the literature15. This approach assumes that afforestation competes for land use with other purposes, such as agriculture or housing. However, some afforestation could be integrated with other land uses, such as planting more trees in urban areas or intercropping trees with agricultural crops24. While our approach simplifies these possibilities, it remains consistent with the scale of afforestation required to offset historical and future human emissions. Thus, this simplification does not diminish the overall validity of our findings.

Considerations of the ecological limitations of emissions offsetting through afforestation

Here we offer insights into the literature on the limitations of afforestation as a way of offsetting carbon emissions. Our estimates of required and available land area for afforestation are based on the literature15,24. However, the assumptions and approaches used in this type of work have been questioned26,27,28. For example, as well as having inherent value culturally, for biodiversity and for carbon sequestration, many unforested land areas are not suitable for afforestation due to abiotic limitations29,30. Trees require suitable temperature, moisture, nutrients, aeration, appropriate radiation, and a rooting environment, as well as the absence of adverse soil or climatic conditions. While we ignore these limitations for simplicity in our calculations below, they remain important. Some of the ecological limitations of emissions offsetting through afforestation are explored below.

Plant photosynthesis requires water to fix carbon, and afforestation has been found to affect local hydrology31. Afforestation increases evapotranspiration compared to grasslands or shrublands, potentially leading to lowered water tables and reduced stream flows32. If water availability is limited, any afforestation efforts may lead to ineffective carbon sequestration and limited offsetting potential.

Trees and other plants require nitrogen, phosphorous, potassium and other essential micronutrients to grow and sequester carbon. Nutrient availability influences a whole range of ecosystem functions, including plant growth and carbon cycling33. Soil nutrient status in natural or seminatural ecosystems have developed over centuries to millennia through natural biogeochemical processes such as pedogenesis (soil formation) and weathering. For example; most parts of the tropics are phosphorus-limited and many temperate and high-latitude ecosystems are nitrogen-limited34,35. Because of this, insufficient nitrogen and/or phosphorous may limit the biomass increase and carbon sequestration potential of afforestation in nutrient-limited areas36. Furthermore, long-term increased nutrient demands from afforestation can lead to decreased soil nutrient availability, thereby exacerbating nutrient limitation within the ecosystem37,38. The introduction of trees, with high productivity and nutrient demands, into nutrient-limited ecosystems can introduce nutrient foraging or mining by symbiotic mycorrhizal fungi. Mycorrhizal fungi associations increase the nutrient supply to trees, but may lead to the breakdown of complex organic matter containing both essential nutrients and carbon. This carbon is then more vulnerable to be lost into the atmosphere through microbial decomposition, resulting in a loss of carbon from the soil in some forested areas39,40. Therefore, nutrient availability and the effect of afforestation on nutrient cycling must be carefully considered when planning afforestation projects to ensure the intended carbon sequestration outcomes and to avoid unintended consequences on ecosystem nutrient cycling.

In areas with high pre-existing soil carbon stores such as, peatlands, tundra or moorlands, afforestation may result in the loss of stored carbon to the atmosphere, likely due to changes in the soil microbial community and nutrient requirements of trees39,41,42.

Even when afforestation projects successfully sequester carbon, that tree biomass carbon store is temporary and limited to the life of the tree, unless the resulting timber is preserved. Furthermore, carbon stored in tree biomass is also vulnerable to being lost due to extreme weather events such as droughts, fires, or hurricanes, or due to disease and to insect outbreaks. Afforestation may even exacerbate negative climate impacts such as increased fire risk or severity and lowering surface albedo in boreal and arctic regions, leading to increased warming43,44,45.

Afforestation for carbon sequestration and emissions offsetting could pose a risk to food security due to reductions in land available for agriculture and food production. This risk is increased if afforestation becomes an economic alternative to agriculture due to the financial incentives of the offsetting market, resulting in productive agricultural land being converted into forests46. Several recent studies have found that land-based climate mitigation can put high levels of strain on food security47,48,49. There is widespread agreement that climate stability should not be achieved at the cost of reduced food security, in line with the United Nations Sustainable Development Goals that promote zero hunger as well as climate action50. However, afforestation and reduction of agricultural land may lead to increasing food prices, reduced food availability and, consequently, negative impacts on populations at risk of hunger46. It is clear that these unintentional yet potentially dangerous side effects of financially incentivised afforestation for emissions offsetting should be considered carefully to avoid causing more harm than good.

The high level of focus on afforestation may erroneously imply that there is a single solution to the climate crisis. There is a growing body of work that suggests that the restoration and protection of peatlands, which store about twice as much carbon as global forest biomass, will play a key role in carbon sequestration and climate change mitigation policy51,52. The role and importance of blue carbon sequestered in oceans, coastal ecosystems and mangroves is gaining increasing recognition53,54. All of the various nature-based solutions to fight climate change and sequester carbon are likely to have positive impacts if they are carried out in a considered, ecologically and socially robust manner.

Results

Estimates of financial limits to offsetting and the Net Environmental Valuation of fossil fuel companies

Fossil fuel companies sell oil, coal and gas. This produces positive economic value. But while doing so, they also generate CO2, which economists call a negative externality. Externalities have been subject to a large literature55. Here we asked, what would be the value of these companies if they had to compensate financially for this externality? The value of a company is determined by its assets net of liabilities. For fossil fuel companies, assets include buildings, extraction machines and to a large part, fossil fuel reserves. Liabilities include loans, bonds issued and debt to shareholders. What is not accounted for in the liabilities of fossil fuel companies is the cost of offsetting their carbon emissions. Here we calculated the valuation of fossil fuel companies, net of that externality. That is their value if they had to fully compensate for the CO2 from burning their reserves (see the methods section for discussions of the limitations of this approach).

We refer to this metric as the Net Environmental Valuation. The Net Environmental Valuation represents the value of a fossil fuel company after subtracting the cost of offsetting its future emissions. This conceptual valuation is not a market valuation but helps understand the extent to which fossil fuel companies can bear environmental externalities. If a company’s Net Environmental Valuation is negative at a given carbon price, it indicates that its societal value is negative. Currently, fossil fuel companies are not taxed on their scope 3 emissions (or the burning of the fossil fuel they extract), nor do they typically offset these emissions, though some do offset scope 1 emissions (emissions occurring during the extraction process). The Net Environmental Valuation explores the potential impact on a company’s value if they were to offset scope 3 emissions or if a tax on these emissions were implemented. A strong assumption we make in this article is that fossil fuel companies would have to offset only downstream emissions from the product they sell (scope 3 emissions), and not their direct emissions from running their companies (scope 1 and 2 emissions), which are excluded from this study. Scope 3 emissions are the most important for fossil fuel companies, and they are therefore crucial for a successful transition. This is why we focus exclusively on these emissions.

Although the Net Environmental Valuation has no direct practical applications, it can be likened to a provision for liabilities in accounting. For example, a car manufacturer might set aside provisions for potential lawsuits. Similarly, if a global carbon tax on scope 3 emissions were established or if fossil fuel companies chose to offset these emissions, they would likely record a corresponding liability. The Net Environmental Valuation estimates the company’s value after accounting for this potential cost. It is calculated by subtracting the cost of offsetting future CO2 emissions from the company’s market capitalization, providing a new perspective on the valuation of fossil fuel companies. It is calculated as follows:

To estimate the offsetting cost of fossil fuel companies, we operate in two steps. First, we rely on estimates by Fossil Free Funds of the potential future CO2 in the balance sheet of fossil fuel companies. The database contains data about the 200 companies owning the most fossil reserves (underground proven reserves, not burned or sold yet).

We do not choose a price of carbon in this paper, but there are estimations of what a tonne of CO2 should cost to its emitter. The most used is the social cost of carbon. It calculates the marginal cost of the impacts resulting from emitting an additional tonne of carbon. There are different estimates available. Estimates of the social cost of carbon are at around $185 per tonne of CO220. The US Inflation Reduction Act used a measure of $180 and the latest estimates by the Environmental Protection Agency (EPA) in the United States have set it at $190. We will use this last figure in the next section. Note that our approach comes with many limitations, which are all outlined in the methods section.

Keeping these limitations in mind, we run a simulation at prices from 0 to $150 as offsetting prices to find at which point all fossil fuel companies in our sample reached a negative Net Environmental Valuation. Note that as 150$ is under the social cost of carbon (around 190$), our findings also apply to the social cost of carbon.

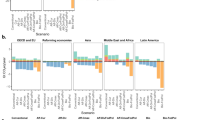

CO2 offsetting pricing has led to a large literature56,57,58. But here we take an approach requiring no a priori knowledge on carbon offsetting prices. We simulate carbon offsetting prices to find the point at which current major fossil fuel companies all reach a negative Net Environmental Valuation. At an offset price of $1/TCO2e, 26% of companies reach a negative Net Environmental Valuation, at $8/TCO2e, 50% of companies, and at $150/TCO2e no company has a positive Net Environmental Valuation (Fig. 1).

For prices ranging from $1/tCO2 to $150/t CO2, the percentage of companies in the 200 largest traded fossil fuel companies that have a negative Net Environmental Valuation was evaluated. At $150/t CO2, all fossil fuel companies have a negative Net Environmental Valuation. At the social cost of carbon (around 190$), all fossil fuel companies also have a negative Net Environmental Valuation.

In the methods section, we analyse actual market offsetting prices. Our reference price for afforestation is $16 per tonne of CO2e. To estimate a carbon market price, we use the 2022 average cost of CO2 on the European ETS carbon offsetting market, which is $83. The European market is the largest offsetting market in the world and hence gives a good sense of a carbon price. For direct air capture, we rely on the current price of around $1000 per tonne for direct air capture by an existing and running offsetting plant in Iceland. We used these three reference prices to assess the Net Environmental Valuation of fossil fuel companies. Afforestation is the cheapest, with the OECD estimating the cost starting at $16 per tonne of CO2e. At this cost, 36% of the companies in our data set would still have a positive market valuation if they tried to offset all the potential emissions of their current reserves (64% of companies would have a negative valuation). Using the 2022 average European carbon market price ($83), 95% of the companies would have a negative Net Environmental Valuation. Finally, using direct air capture at the current cost of the technology ($1000), all companies in the dataset would have a Net Environmental Valuation.

Aggregating the company results to global estimates offers perspective. If we sum up the total market capitalisation of the 200 largest oil, gas and coal companies in our sample, we get a total value for these companies of $7.01 trillion. But if we wanted to pay for the offsetting of these companies, it would cost $10.8 trillion (tree offsetting), $59.29 trillion (ETS Carbon Market) or $673.7 trillion (current direct air capture technology). These numbers are 11%, 62% and 701% of global GDP (see calculations in the methods section). This means that offsetting emissions of current reserves of fossil companies with direct air capture would cost up to seven years of global human economic production. All wealth generated by humans globally during a 7-year period would have to be reinvested into carbon offsetting. Looking at the cost of offsetting, the takeaway is that it is likely be more effective to stop these emissions in the first place rather than offsetting them.

Even if direct air capture technology drops to 150$/t CO2e, the Net Environmental Valuation of fossil fuel companies would still be negative. Our survey in the methods section shows an average of studies estimating the price of direct air capture at around 400$/tCO2e (with a range from 94–1000$/tCO2e). This means that if fossil fuel companies were to offset their emissions, direct air capture would unlikely offer a financially viable solution. The cheapest solution in monetary terms (afforestation), offsetting all current fossil fuel companies proven reserves, would still cost $11 trillion with 36% of the largest fossil fuel companies having a negative Net Environmental Valuation. And this does not include the cost of acquiring the land required.

Looking at the largest fossil company in the world, Saudi Aramco, the valuation of the company at the time of writing is $2.2 trillion. Offsetting its reserves with afforestation would make its value be divided by four to only $482.9 billion. If it had to offset its emissions at the ETS average price at 83$, it would drop to a negative value of $6.6 trillion. If it were to offset its emissions at the current cost of direct air capture ($1000), the value of the company would fall at a staggering -$103.9 trillion (or a bit more than global GDP for comparison). This shows that offsetting is not an option for Saudi Aramco or any of the companies in our sample.

While our estimates consider the real market cost of offsetting, we can also compute the Net Environmental Valuation of fossil fuel companies against the social price of carbon. This is not a market value like the prices we used before. Yet, it is a good measure of the current estimate of policymakers for the cost of emitting an additional tonne of carbon. If we use any of these suggested prices for the social cost of carbon (180–190 for 2022), the Net Environmental Valuation of fossil fuel companies goes to 0. Put another way, if we think the social cost of carbon is at the right level, running a fossil fuel company is not a financially viable enterprise. Or if a government wanting to run one of these companies did a cost-benefit analysis, it should decide against running the company at this level of social cost of carbon. For now, the social cost of carbon has been mostly used for public investment projects. As Fig. 1 shows, any social cost of carbon above $150 leads to the conclusion that running a fossil fuel company generates negative value for society.

Spatial limitations of emissions offsetting through afforestation

We provide estimates of the surface needed for afforestation by the largest fossil fuel companies (Fig. 2). The largest 200 fossil fuel companies own 672Gt CO2e in reserves. How much space is needed to offset this CO2 by afforestation? We get a sense of the global carbon capture potential by estimating the maximum potential capture by afforestation on our planet. We also compare the potential future emissions from the reserves of the largest fossil fuel companies in different countries to get a sense of the scale of offsetting needed. Our approach focuses on afforestation as a natural offsetting method but acknowledges key limitations, such as the limited availability of suitable land and the competing ecological, cultural, and economic values of unforested areas. The simulations presented here abstract from these broader considerations, serving as an upper limit rather than a definitive guideline for offsetting potential. Furthermore, large-scale afforestation may have ecological impacts that could undermine its effectiveness, a topic explored further in the paper (the methods section offers more detailed limitations).

Note: Habitable land is a theoretical construct as given by the difference between total land mass, removing the glacier (10% of the total land mass) and barren land (19% of the total land mass) such as deserts, dry salt flats, beaches, sand dunes, and exposed rocks. The figures are from Hannah Ritchie and Max Roser (2013) - “Land Use”. Published online at OurWorldInData.org. Retrieved from: ‘https://ourworldindata.org/land-use’.

We try to estimate the maximum afforestation potential of our planet. This estimate is given as a hard physical limit of afforestation, not a recommendation. We then use this estimate to give the reader a sense of the space needed to offset future planned emissions by all fossil fuel companies, as well as historical human emissions. We are not the first to produce such estimates. Griscom et al. present a sequestration rate of 10.3 GtCO2/year using 678 Mha by 2030, Lewis et al. find 154 GtCO2 on 350 Mha over a time period of 70 years, and Bastin et al. show a potential of 752 GtCO2 using 900 Mha without specifying a time period24,59,60. However, this last number is disputed61,62 and it would potentially take over 100 years. Our contribution, however, is to offer a maximum rather than a realistic estimate. This shows the limitation of offsetting, which is the focus of this paper.

We ask a theoretical and abstract question, to better understand the issue with offsetting by afforestation. How much CO2 can our planet absorb through afforestation by 2050? And how much space is needed to offset future potential fossil fuel and past emissions through afforestation? To do this, we ran a thought experiment to show the maximum offsetting potential of our planet. We ask, how much CO2 could our planet absorb if we removed everything (cities, roads, agricultural land, existing forest and everything that is on land), and replaced it with trees. This is of course, not realistic, but doing so gives us the maximum offsetting potential of our planet. Part 6 of the method section gives the step-by-step calculations. Put simply, we take regional offsetting potential per hectare from the literature, and multiply it by the space on all continents, except Antarctica15. We use this to generate a total offsetting estimate for Earth's total land surface as well as an estimate per km2.

We then use this last metric to compare the space needed with the size of different countries. Our comparisons in Fig. 3 (a and b) offer an idea of what the offsetting requirements represent in geographical terms. Offsetting all the emissions of all reserves of the 200 largest fossil fuel companies would take more land area than that of North America and part of South America. (panel a). And if we tried to offset historical emissions from fossil fuel and cement, all agricultural land would have to be replaced by forests from now until 2050. In terms of land, it would cover all of North America, Western Europe and around three quarter of Africa (panel b). Note that these figures are not realistic, they are a representation. Think of them as an artist sketch. They are wrong as they suggest afforestation in places where trees cannot be planted, such as mountain tops, deserts or lakes. Their point is only to give the reader a visual understanding of the scale of the space needed to offset planned and past emissions. They are also very rough approximations, though, as explained in the many assumptions of this paper, likely a lower band.

Panel a shows the afforestation surface needed to offset future emissions of fossil fuel companies (measured as the emission potential of their reserves). Panel b shows the afforestation surface needed to offset historical human emissions. Note: data for afforestation per continent from Bernal et al.15 (see also the appendix, Table A6). Land surface’ data from the United Nation for each country. The first map represents afforestation for future emissions which are estimates around 673 and the surface on the map would offset 673,70 GT CO2. Historical emission are estimated around 1732.37 and the area on the map would offset 1732.43 GT CO2. The slight mismatch is due to the fact that we only color entire countries on the map. Note that the surface is a simplification as it include all land on this surface, including barren land, mountain ranges or lakes. This is why this is not an accurate map but only a visual representation to give an order of magnitude.

Discussion

In this paper we showed the financial, spatial and ecological limitations of carbon offsetting. The issue is important as most climate scenarios include offsetting, alongside reduction in emissions. We focused mostly on fossil fuel companies, as they have started to communicate about offsetting as a solution to CO2 emissions. While our findings come with many limitations and simplifications outlined in the paper and methods section, we offer global estimates of the practical limitations of carbon offsetting.

We show that there are financial limits to offsetting. If we take an offsetting price of the current price on the European ETS market (around $83 for 2022), 95% of fossil fuel companies would have a negative market value (we called it Net Environmental Valuation). If we wanted to offset the current fossil fuel reserves with afforestation by 2050, it would require afforestation on the equivalent whole of North America, necessitating the removal of all existing infrastructure, agricultural land, and urban areas. This would offset around 590 Gt CO2, while fossil fuel companies have reserves that could generate 674 Gt CO2. To offset all human historical emissions from fossil fuel and cement, more than half of our habitable land (or all non-barren land) would have to be covered by trees.

We show that even if afforestation has climate benefits, there are also many risks and limitations. Nutrient availability, water supply, temperature, soil suitability, and the suitability of different areas for afforestation should be carefully considered. Carbon stored in trees is temporary, vulnerable to loss due to extreme weather events, and must be preserved to retain sequestered carbon. In addition, afforestation for carbon sequestration could affect food security due to the reduction in land available for agriculture and the negative consequences of afforestation to biodiversity, as it mainly involves monoculture.

Fossil fuel companies are becoming more engaged with offsetting, and policymakers are increasingly focused on net-zero timelines and negative emissions targets. But what we show in this paper is that there is no way around emissions reduction. Technologies like direct air capture make it prohibitively expensive to extract fossil fuel in the first place and offset it later, even within the next decades. Afforestation, while financially more viable, poses unsurmountable challenges of land use and ecological limitations, in a world with a growing population in need of more living space and agricultural land. In short, it is economically cheaper to stop extracting fossil fuel than to burn it an offset it later when the social cost of carbon is taken into account.

While we show that the priority is on emission reduction over naïve offsetting, this does not mean that forest conservation and restoration should not be a policy objective in and of themselves. Forests play a critical role in reducing human impact by sequestering carbon, conserving biodiversity, and maintaining ecological functions essential for life on earth. These natural climate solutions, though not a substitute for offsetting large-scale emissions, are indispensable for addressing the multifaceted challenges of climate change and achieving a sustainable future.

Methods

Limitations, important simplifications and caveats – financial limits

Our approach relies on a few important simplifications. The assumption is that fossil fuel companies would have to offset only downstream emissions from the product they sell (scope 3 emissions), and not their direct emissions from running their companies (scope 1 and 2 emissions), which are excluded from this study. Scope 3 emissions are the most important for fossil fuel companies, and they are therefore crucial for a successful transition. This is why we focus exclusively on these emissions. Also, we assume that fossil fuel companies would use all their fossil fuel reserves. This is because in terms of company valuation, the value of fossil fuel companies includes all assets and because fossil fuel companies are trying to burn as much of these reserves as they can63. But regulation or other factors could stop them from using all their reserves.

Another important caveat needs to be kept in mind when interpreting our results. We use potential emissions from reserves, and fossil fuel companies do not have as much control over these emissions as they do over the ones during their production process, for example. Another limitation of our Net Environmental Valuation is it that it only considers greenhouse gas emissions of fossil fuel companies. The impact of these companies on nature is much broader and also includes land use and other pollutions which are overlooked in this study. Our estimates of Net Environmental Valuation might also be too optimistic. Even companies with a positive Net Environmental Valuation might still not be liable to operate their business. A company having to pay as much as half of its entire market value in offsetting costs is likely to go bankrupt as well. Finally, also biasing our estimation downward, is that our afforestation cost does not include land purchase. An afforestation project in Manhattan would cost more than $16 per tonne if land had to be purchased first. Despite all these caveats, our estimates are a first simple attempt at internalizing the carbon externality of fossil fuel companies.

There are issues with using the market valuation in the Net Environmental Valuation. Investors might already have priced in part of the price of carbon or offsetting. If investors believe that regulators will limit the use of fossil fuel, they will discount the value of fossil fuel companies. While this is a possibility, it is unlikely to be a short term possibility, as fossil fuel companies and investors know that demand for fossil is unlikely to drop globally over the next few decades64.

Note that our database from Fossil Free Funds only presents data of proven reserves (1P) for ranking oil and gas companies. Proven reserves are the ones that are 90% likely to be extracted soon, usually in 10–15 years. Probable reserves have a 50% chance of extraction, but they are excluded from this exercise. This means our calculations here are closer to lower band. For coal, Fossil Free Funds uses the latest reported coal reserves from the S&P Global Database, after a reasonableness check. These reserves are the mineable part of a resource. They assign reserves to listed companies based on their ownership of each mine.

Limitations, important simplifications and caveats – spatial limits

Before diving into the approach presented here, let us first list some simplifying assumptions and limitations to our approach (in addition to the ones presented in the methods section for the first part). One limitation of our approach is to only use trees as natural offsetting methods. Offsetting by peatland restoration can likely generate better outcomes than afforestation, but estimates are harder to find and the practice is not available at a large scale commercially yet. It may not be feasible at a large scale due to climatic and hydrological limitations. Also, we only consider single offsetting projects. This assumes that all afforestation projects would never revert back to another land use, which is unlikely to be the case and will bias our estimates downward65.

One major limitation of afforestation as a means of emissions offsetting is the availability and suitable land area. This breaks down into several key areas including; physical land area available, land suitable for tree growth, conflicts with other land-uses or ecosystem types and important food security implications. There is land on Earth where afforestation is possible, but this land often belongs to someone. Ownership can be understood in a legal sense, but it can also be functional or emotional66. Land is rarely unutilised or devoid of ecological, cultural, or economic value. It often serves a purpose for humans or animals, even when they do not have formal ownership of it. Unforested land has inherent value culturally, for biodiversity, ecosystem services and for carbon sequestration, which should not be forgotten29,30. Because of this it is important to take a broad ecological perspective on landscape restoration67. We abstract from these considerations here to only focus on the surface needed, but these limitations would of course also play a role in the applicability of these offsetting simulations presented here. The simulations presented are therefore more of an upper limit of what can be done than a guideline. Furthermore, afforestation would need to be implemented at a scale which is likely to have ecological impacts that may undermine such offsetting efforts36. We further explore the ecological limits of afforestation for carbon sequestration in the literature section in the body of the paper.

Caclulations of the cost as a percentage of world GDP

The paper offers estimates of offsetting cost in percentage of GDP, here are how these are calculated (Table 1). It is understood that, if the cost would be incurred, it would affect GDP and hence there would never be a cost going above GDP. These are given only as a benchmark in the same sense debt to GDP ratio are given for example.

Carbon offsetting price data overview

One of the goals of the paper is to have an understanding of the market value of carbon offsetting. This is the cost you would have to pay today if fossil fuel companies wanted to offset emissions. This price is likely to evolve if there is new offsetting technology available. The price might also increase if there is more demand for offsetting, regardless of the technologies. Here we refrain from making projections of the future. Instead, we aim to empirically find a wide range of available carbon prices. This range can then be compared with the results in the main body of the paper, where we look at Net Environmental Valuation of fossil fuel firms for up to $150.

Below is our review of the different prices for our three offsetting methods: tree plantation, compensation certificate purchase on the European ETS market and direct air capture compensation. The point of our offsetting cost search is to have a realistic lower, middle and upper band and a mix of technologies. Our analysis in the main paper provides estimates for any price from 0 to $150.

Afforestation or tree plantation

The cost of planting trees is estimated in a meta study between 10 and 100$/tCO2 in the United States68. The OECD estimates the cost of forest conservation around 4–9$/tCO2 and 16–25$/tCO2 for afforestation69. In simulations, estimates between $5 and $100 are used70. We take the value of $16 from the OECD as a lower band.

Carbon market price: the price of the European Union Emissions Trading System 83.02$/tCO2

The European Union Emissions Trading System (EU ETS) is a CO2 trading mechanism. It allows companies that generate less CO2 than plan to sell excess CO2 generation capacity. It is labelled as a “cap and trade” system, where the legislator sets a maximum CO2 cap and private market participants can then trade these rights to emit CO2. Trading happens on a centralised market, which allows to have a daily price of carbon.

European market price (an average of $83.02 in 2022, as of 20.07.2022): Companies exchange their emissions quotas on a carbon market with each other. They pay for the “extra” emissions caused by their activity, which is a form of compensation or offsetting.

Direct air capture

Carbon capture and storage is a technology that involves the removal and storage of CO2 directly from the atmosphere. There are several technologies and research on the topic evolve fast. Here we offer a non-exhaustive review of prices we found to give a bracket of prices for direct air capture (Fig. 4). Direct air capture also provides us with an upper band price that we use in this paper. This price is based on the cost of offsetting carbon today at the Ocra plant run by CIimeworks, as this is one of the few sources of offsetting available today.

The figure shows the mean, median, min and max for direct air capture offsetting costs.

Note that direct air capture is also limited as it is not possible to directly capture CO2 emissions produced by long-distance aviation and marine transport71.

Table 2 below provides a quick overview of the prices we found from existing projects or from estimates in the literature. The literature also offers a projection of around 200 USD/tCO2 by around 205072. This would mean that according to their projection, even by 2050 technology would not allow for a positive Net Environmental Valuation for the fossil fuel companies analysis.

Looking at Fig. 1 in comparison, we can see that the largest part of direct air capture fall outside of the $150 limit by which all fossil fuel companies attain a negative Net Environmental Valuation. In other term, regardless of direct air capture or technology, all fossil fuel companies would have a negative Net Environmental Valuation.

Data in this analysis comes from a discussion on the potential of direct air capture technology to transform atmospheric carbon dioxide into usable products (https://singularityhub.com/2019/08/23/the-promise-of-direct-air-capture-making-stuff-out-of-thin-air/). The International Energy Agency (IEA) has also addressed direct air capture in detail, highlighting its possible contributions to climate mitigation (https://www.iea.org/reports/direct-air-capture). Currently, however, the technology remains costly, with an estimated expense of around €1000, which is roughly equivalent to $1000 at recent exchange rates (https://www.ft.com/content/8a942e30-0428-4567-8a6c-dc704ba3460a).

Afforestation space needed for each fossil fuel company

Capture Rate database

We combine data from Bernal et al.15 on land offsetting potential with the data from Bastin et al.24 on available land for tree plantation. This last figure is compiled by the author for each country based on satellite pictures and a machine learning algorithm. Bernal et al.15 provided us with data about the area available for Forest Landscape Restoration (FLR) Activities. FLR activities are activities that can be carried out in order to restore vegetation in an area such trees plantation, natural regeneration, agroforestry, mangrove regeneration and mangrove shrub. The paper also provided us with the carbon capture rate (amount of CO2 that could be absorbed by the vegetation from an FLR activity) by year for each activity in tCO/year/ha (a range of the 20 first years, then another of the 40 following years), and these in 3259 regions in 177 countries. To get countries estimates for the capture rates, we assessed an average weighted by the available area for FLR Activities in each region. Then we obtained a dataframe containing the average capture rates for FLR Activities in each country.

Calculation of the surface needed for compensation

To calculate the surface needed, we used estimates from the capture rates database we created. We computed the surface needed by 2050 (in 27 years) as this is the date of many net-zero pledges, either by fossil fuel companies themselves, or by governments that regulate them. We also do another estimation over the lifecycle of a hectare of forest based on an estimate by (Bernal et al.15 The idea behind this second assumption is that an afforested or reforested plot of land will be a carbon sink until maturity. At maturity, our model here assumes that absorption stops, and that the hectare has a net-zero effect as a carbon sink. This is a simplification, but it allows for a clear model.

Our data is based on the following calculation made for each company’s underground reserve:

Maximum global offsetting calculations

This section explains in details of how offsetting estimates are generated. These estimates rely on heavy assumptions. They are therefore to be taken with a lot of caution. If anything, they represent a maximum capture potential of the planet, more than a realistic policy to be implemented.

First, we take estimates of carbon capture by geography generated by Bernal et al.15 Table 3 reproduces these from the original source, along with the 95% confidence interval.

Table 4 takes these numbers and multiplies them by the number of years until 2050. So that is 20 years at the growth rate from trees from 0–20 years estimated by Bernal et al.15 and then 5 years at the rate 20–60 (accounting for the 25 years between 2025 and 2050). This is the amount per hectare that trees in different regions can absorb until 2050. Note that here we assume that all these projects will not be stopped by 2050, which is unlikely. This makes this number an overstatement.

The next table, Table 5, then groups the different regions to get their CO2 capture potential. Here, there are two important simplifications. First, we take the total landmass of these regions. We ignore anything that is already present on the land surface of these continents. This could be agricultural land, cities or other types of surfaces. It also excludes the fact that some of these landmasses might not be able to welcome trees. Again, the idea here is to reach a maximum offsetting potential rather than a recommended or realistic offsetting measure. The second simplification is that we take the average for each continent between the humid and dry capture potential. While this is a gross oversimplification, taking only dry or only humid does not fundamentally change the results. We then take the total of the different continents to obtain a global potential CO2 capture for the entire planet. Note that all estimates exclude Antarctica, which is unlikely to have much of a CO2 capture potential by afforestation.

The total obtained of 4300 is the absolute maximum that our planet could offset by 2050. Note that this number is also limited by the fact that it would imply replace current forests with new forests, which is likely to offset CO2. But again, this number is an absolute physical maximum.

We also ran the same simulation until 2083, or 60 years from now. This is the maximum CO2 capture potential according to Bernal et al.15. The idea is that a forest would stop being a net CO2 sink after 60 years. Imagine that trees would start to decompose and emit the CO2 that they have captured into the atmosphere again. The maximum capture potential on the Earth’s landmass by 2083 is 8 092.35 (±1 354.3).

Finally, in an effort to make these numbers more relatable, we compare them to existing land surfaces. This last exercise is done only to give the reader an intelligible comparison. To do this, we take the value of the average global capture potential by 2050. This number is in 5. It is 4086 Gt CO2 for 136,055,876 km2. Or 30,033 T CO2 per km2. We then compare, for illustration only, this number to surfaces known to the reader: countries. We also compare this to surfaces linked to human land use, such as total agricultural surface, built land and so on.

Global historical CO2 emissions data

Data from the Global Carbon Project (2022) offers global estimates of human emissions from fossil fuel and cement since 18502. They estimate global CO2 production at 472807.73 Mt of carbon, or 1732367.51 Mt CO2 or 1732.37 Gt CO2 since 1850. While there were emissions from the burning of fossil fuels from 1750 to 1850, these data offer a good approximation for global human emissions from the burning of fossil fuel and cement production.

Data availability

The datasets used in this study include financial data on fossil fuel company valuations, estimates of fossil fuel reserves, and carbon sequestration potential. The fossil fuel reserve data were sourced from the Carbon Underground 200 dataset, which is proprietary to Fossil Free Funds. Financial valuation data, including market capitalization figures, are primarily available from publicly accessible market reports, but the specific data used in this study were obtained from Refinitiv, which is proprietary. Processed datasets supporting the findings of this study have been deposited in SocArXiv and are accessible at https://osf.io/xuyvn/ or https://doi.org/10.17605/OSF.IO/XUYVN. Due to licensing restrictions, the original reserve and market capitalization data cannot be shared directly, but they can be accessed through Fossil Free Funds (https://fossilfreefunds.org) and Refinitiv (https://www.refinitiv.com/en) by those with the appropriate access rights. Additional model output data and calculations have been uploaded to SocArXiv at https://osf.io/xuyvn/ or https://doi.org/10.17605/OSF.IO/XUYVN. All other relevant data used in this study are included in the manuscript. The data are also available as supplementary data 1.

References

Global Carbon Budget. Global Carbon Budget 2023. (2023).

Friedlingstein, P. et al. Global Carbon Budget 2021. Earth Syst. Sci. Data 14, 1917–2005 (2022).

Shell. Shell accelerates drive for net-zero emissions with customer-first strategy. https://www.shell.com/media/news-and-media-releases/2021/shell-accelerates-drive-for-net-zero-emissions-with-customer-first-strategy.html (2021).

Dargusch, P. & Thomas, S. A critical role for carbon offsets. Nat. Clim. Change 2, 470–470 (2012).

Mackey, B. et al. Untangling the confusion around land carbon science and climate change mitigation policy. Nat. Clim. Change 3, 552–557 (2013).

Wade, B. & Rekker, S. Research can (and should) support corporate decarbonization. Nat. Clim. Change 10, 1064–1065 (2020).

Anderson, K. & Peters, G. The trouble with negative emissions. Science 354, 182–183 (2016).

Bellamy, R. Incentivize negative emissions responsibly. Nat. Energy 3, 532–534 (2018).

van Vuuren, D. P., Hof, A. F., van Sluisveld, M. A. E. & Riahi, K. Open discussion of negative emissions is urgently needed. Nat. Energy 2, 902–904 (2017).

Rogelj, J. & Lamboll, R. D. Substantial reductions in non-CO2 greenhouse gas emissions reductions implied by IPCC estimates of the remaining carbon budget. Commun. Earth Environ. 5, 1–5 (2024).

González-Mahecha, E., Lecuyer, O., Hallack, M., Bazilian, M. & Vogt-Schilb, A. Committed emissions and the risk of stranded assets from power plants in Latin America and the Caribbean. Environ. Res. Lett. 14, 124096 (2019).

Welsby, D., Price, J., Pye, S. & Ekins, P. Unextractable fossil fuels in a 1.5 °C world. Nature 597, 230–234 (2021).

Semieniuk, G. et al. Stranded fossil-fuel assets translate to major losses for investors in advanced economies. Nat. Clim. Change 12, 532–538 (2022).

Macaire, C., Grieco, F., Volz, U. & Naef, A. High Voltage: Financing the Path to Zero Coal. Work. Pap. (2024).

Bernal, B., Murray, L. T. & Pearson, T. R. H. Global carbon dioxide removal rates from forest landscape restoration activities. Carbon Balance Manag. 13, 22 (2018).

Environmental Protection Agency. Social cost of carbon. U. S. Environ. Prot. Agency EPA Wash. DC USA (2013).

Prest, B. C., Rennert, K., Newell, R. G., Pizer, W. A. & Anthoff, D. Updated Estimates of the Social Cost of Greenhouse Gases for Usage in Regulatory Analysis. Resources for the Future (2023). Available at: https://www.rff.org/publications/testimony-and-public-comments/updated-estimates-of-the-social-cost-of-greenhouse-gases-for-usage-in-regulatory-analysis/.

Nordhaus, W. D. Rolling the ‘DICE’: an optimal transition path for controlling greenhouse gases. Resour. Energy Econ. 15, 27–50 (1993).

Nordhaus, W. D. Revisiting the social cost of carbon. Proc. Natl. Acad. Sci. 114, 1518–1523 (2017).

Rennert, K. et al. Comprehensive evidence implies a higher social cost of CO2. Nature 610, 687–692 (2022).

Coffin, M. & Grant, A. Beyond Petrostates: The burning need to cut oil dependence in the energy transition. Carbon Tracker https://coilink.org/20.500.12592/80gb82f (2021).

Solano-Rodríguez, B. et al. Implications of climate targets on oil production and fiscal revenues in Latin America and the Caribbean. Energy Clim. Change 2, 100037 (2021).

Welsby, D., Rodriguez, B. S., Steve, P. & Vogt-Schilb, A. High and Dry: Stranded Natural Gas Reserves and Fiscal Revenues in Latin America and the Caribbean. https://doi.org/10.18235/0003727 (2022).

Bastin, J.-F. et al. The global tree restoration potential. Science 364, 76–79 (2019).

Mo, L. et al. Integrated global assessment of the natural forest carbon potential. Nature 624, 92–101 (2023).

Friedlingstein, P., Allen, M., Canadell, J. G., Peters, G. & Seneviratne, S. I. Comment on “The global tree restoration potential”. Front. Ecol. Environ. 366, eaay8060 (2019).

Lewis, S. L., Mitchard, E. T. A., Prentice, I. C., Maslin, M. & Poulter, B. Comment on “The global tree restoration potential”. Science 366, 5–8 (2019).

Veldman, J. W. et al. Comment on “The global tree restoration potential”. Science 366, 1–5 (2019).

Veldman, J. W., Silveira, F. A. O., Fleischman, F. D., Ascarrunz, N. L. & Durigan, G. Grassy biomes: An inconvenient reality for large-scale forest restoration? A comment on the essay by Chazdon and Laestadius. Am. J. Bot. 104, 649–651 (2017).

Bengtsson, J. et al. Grasslands-more important for ecosystem services than you might think. Ecosphere 10, e02582 (2019).

Nosetto, M. D., Jobbágy, E. G., Brizuela, A. B. & Jackson, R. B. The hydrologic consequences of land cover change in central Argentina. Agric. Ecosyst. Environ. 154, 2–11 (2012).

Farley, K. A., Jobbágy, E. G. & Jackson, R. B. Effects of afforestation on water yield: a global synthesis with implications for policy. Glob. Change Biol. 11, 1565–1576 (2005).

Fernández-Martínez, M., Vicca, S., Janssens, I. A., Campioli, M. & Peñuelas, J. Nutrient availability and climate as the main determinants of the ratio of biomass to NPP in woody and non-woody forest compartments. Trees 30, 775–783 (2016).

Sjögersten, S. & Wookey, P. a. The role of soil organic matter quality and physical environment for nitrogen mineralization at the forest-tundra ecotone in Fennoscandia. Arct. Antarct. Alp. Res. 37, 118–126 (2005).

Turner, B. L., Brenes-Arguedas, T. & Condit, R. Pervasive phosphorus limitation of tree species but not communities in tropical forests. Nature 555, 367–370 (2018).

Smith, L. J. & Torn, M. S. Ecological limits to terrestrial biological carbon dioxide removal. Clim. Change 118, 89–103 (2013).

Berthrong, S. T., Jobbágy, E. G. & Jackson, R. B. A global meta-analysis of soil exchangeable cations, pH, carbon, and nitrogen with afforestation. Ecol. Appl. 19, 2228–2241 (2009).

Näsholm, T. et al. Are ectomycorrhizal fungi alleviating or aggravating nitrogen limitation of tree growth in boreal forests?. New Phytol. 198, 214–221 (2013).

Friggens, N. L. et al. Tree planting in organic soils does not result in net carbon sequestration on decadal timescales. Glob. Change Biol. 26, 5178–5188 (2020).

Clemmensen, K. E. et al. A tipping point in carbon storage when forest expands into tundra is related to mycorrhizal recycling of nitrogen. Ecol. Lett. 24, 1193–1204 (2021).

Hartley, I. P. et al. A potential loss of carbon associated with greater plant growth in the European Arctic. Nat. Clim. Change 2, 875–879 (2012).

Parker, T. C., Subke, J. A. & Wookey, P. A. Rapid carbon turnover beneath shrub and tree vegetation is associated with low soil carbon stocks at a subarctic treeline. Glob. Change Biol. 21, 2070–2081 (2015).

Betts, R. A. Offset of the potential carbon sink from boreal forestation by decreases in surface albedo. Nature 408, 187–190 (2000).

Veldman, J. W. et al. Where tree planting and forest expansion are bad for biodiversity and ecosystem services. BioScience 65, 1011–1018 (2015).

Hermoso, V., Regos, A., Morán-Ordóñez, A., Duane, A. & Brotons, L. Tree planting: A double-edged sword to fight climate change in an era of megafires. Glob. Change Biol. 27, 3001–3003 (2021).

Doelman, J. C. et al. Afforestation for climate change mitigation: Potentials, risks and trade-offs. Glob. Change Biol. 26, 1576–1591 (2020).

Frank, S. et al. Reducing greenhouse gas emissions in agriculture without compromising food security?. Environ. Res. Lett. 12, 105004 (2017).

van Meijl, H. et al. Comparing impacts of climate change and mitigation on global agriculture by 2050. Environ. Res. Lett. 13, 064021 (2018).

Hasegawa, T. et al. Risk of increased food insecurity under stringent global climate change mitigation policy. Nat. Clim. Change 8, 699–703 (2018).

UN G.A., U. N. G. A. Transforming Our World: The 2030 Agenda for Sustainable Development (2015).

Humpenöder, F. et al. Peatland protection and restoration are key for climate change mitigation. Environ. Res. Lett. 15, 104093 (2020).

Bradfer-, T. et al. The potential contribution of terrestrial nature-based solutions to a national ‘ net zero ’ climate target. J. Appl. Ecol. 1–12 https://doi.org/10.1111/1365-2664.14003 (2021).

Rovai, A. S. et al. Global controls on carbon storage in mangrove soils. Nat. Clim. Change 8, 534–538 (2018).

Heinze, C. et al. The ocean carbon sink – impacts, vulnerabilities and challenges. Earth Syst. Dyn. 6, 327–358 (2015).

Nordhaus, W. Climate change: the ultimate challenge for economics. Am. Econ. Rev. 109, 1991–2014 (2019).

Wilson, I. A. G. & Staffell, I. Rapid fuel switching from coal to natural gas through effective carbon pricing. Nat. Energy 3, 365–372 (2018).

Böhringer, C., Fischer, C., Rosendahl, K. E. & Rutherford, T. F. Potential impacts and challenges of border carbon adjustments. Nat. Clim. Change 12, 22–29 (2022).

Klenert, D. et al. Making carbon pricing work for citizens. Nat. Clim. Change 8, 669–677 (2018).

Lewis, S. L., Wheeler, C. E., Mitchard, E. T. A. & Koch, A. Restoring natural forests is the best way to remove atmospheric carbon. Nature 568, 25–28 (2019).

Griscom, B. W. et al. Natural climate solutions. Proc. Natl. Acad. Sci. 114, 11645–11650 (2017).

Waring, B. et al. Forests and Decarbonization – Roles of Natural and Planted Forests. Front. For. Glob. Change 3, 58 (2020).

Veldman, J. W. et al. Comment on “The global tree restoration potential”. Science 366, eaay7976 (2019).

Kenner, D. & Heede, R. White knights, or horsemen of the apocalypse? Prospects for Big Oil to align emissions with a 1.5 °C pathway. Energy Res. Soc. Sci. 102049 https://doi.org/10.1016/j.erss.2021.102049 (2021).

Naef, A. The impossible love of fossil fuel companies for carbon taxes. Ecol. Econ. 217, 108045 (2024).

Groom, B. & Venmans, F. The social value of offsets. Nature 619, 768–773 (2023).

Preston, S. D. & Gelman, S. A. This land is my land: Psychological ownership increases willingness to protect the natural world more than legal ownership. J. Environ. Psychol. 70, 101443 (2020).

Temperton, V. M. et al. Step back from the forest and step up to the Bonn Challenge: how a broad ecological perspective can promote successful landscape restoration. Restor. Ecol. 27, 705–719 (2019).

Richards, K. R. & Stokes, C. A Review of Forest Carbon Sequestration Cost Studies: A Dozen Years of Research. Clim. Change 63, 1–48 (2004).

Grafton, R. Q., Chu, H. L., Nelson, H. & Bonnis, G. A global analysis of the cost-efficiency of forest carbon sequestration, OECD Environment Working Papers, 30 November 2021, https://doi.org/10.1787/e4d45973-en (2021).

Austin, K. G. et al. The economic costs of planting, preserving, and managing the world’s forests to mitigate climate change. Nat. Commun. 11, 5946 (2020).

Fasihi, M., Efimova, O. & Breyer, C. Techno-economic assessment of CO2 direct air capture plants. J. Clean. Prod. 224, 957–980 (2019).

Shayegh, S., Bosetti, V. & Tavoni, M. Future prospects of direct air capture technologies: insights from an expert elicitation survey. Front. Clim. 3, 1–14 (2021).

Tollefson, J. Sucking carbon dioxide from air is cheaper than scientists thought. Nature 558, 173–173 (2018).

Keith, D. W., Holmes, G., Angelo, D. S. & Heidel, K. A process for capturing CO2 from the atmosphere. Joule 2, 1573–1594 (2018).

Keith, D. W., Ha-Duong, M. & Stolaroff, J. K. Climate Strategy with CO2 capture from the air. Clim. Change 74, 17–45 (2006).

Acknowledgements

We are grateful to Muriel Demottais for assistance with data collection. There is no funding acknowledgements by the authors.

Author information

Authors and Affiliations

Contributions

Alain Naef and Nina Lindstrøm Friggens conceptualised the study and developed the methodology. Data curation and formal analysis were carried out by Alain Naef and Patrick Njeukam. All three authors contributed to the investigation. Alain Naef and Nina Lindstrøm Friggens wrote the original draft and led the review and editing process.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Peer review

Peer review information

Communications Earth & Environment thanks Anil Shrestha and the other, anonymous, reviewer(s) for their contribution to the peer review of this work. Primary Handling Editors: Heike Langenberg, Aliénor Lavergne. A peer review file is available.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Naef, A., Friggens, N.L. & Njeukam, P. Carbon offsetting of fossil fuel emissions through afforestation is limited by financial viability and spatial requirements. Commun Earth Environ 6, 459 (2025). https://doi.org/10.1038/s43247-025-02394-y

Received:

Accepted:

Published:

DOI: https://doi.org/10.1038/s43247-025-02394-y